From Speculation to Habit: What Web3 Apps Can Learn From Fintech Retention

The next Web3 winners will not be the teams that acquire the most wallets during an incentive cycle. They will be the teams that retain behavior, capital, and trust after the incentive is gone.

Web3 does not have a simple acquisition problem.

The industry can attract attention. It can create quest participation, social volume, and short bursts of onchain activity. The harder problem starts after that moment.

Do users come back when the points campaign ends?

Do they repeat the core action without a new reward?

Do they keep capital in the product when yields compress, volatility fades, or the narrative moves somewhere else?

That is where many Web3 apps break.

Airdrops, token launches, points, KOL campaigns, and dependence on market cycles are strong at creating first action. They are much weaker at creating durable financial behavior. Broader fintech and wealth management data shows why: financial retention depends on trust, performance, guidance, product access, digital tools, cost clarity, and recurring use.

Web3’s real problem is post-incentive retention

A lot of crypto growth still treats acquisition as the main victory.

A wallet connected. A user claimed. A trade happened. A deposit appeared. A campaign dashboard showed volume. On the surface, the numbers look alive.

But many of those users are not users in the product sense. They are campaign participants, yield seekers, farmers, or speculative visitors. They came for a reason that may have little to do with the product’s long-term utility.

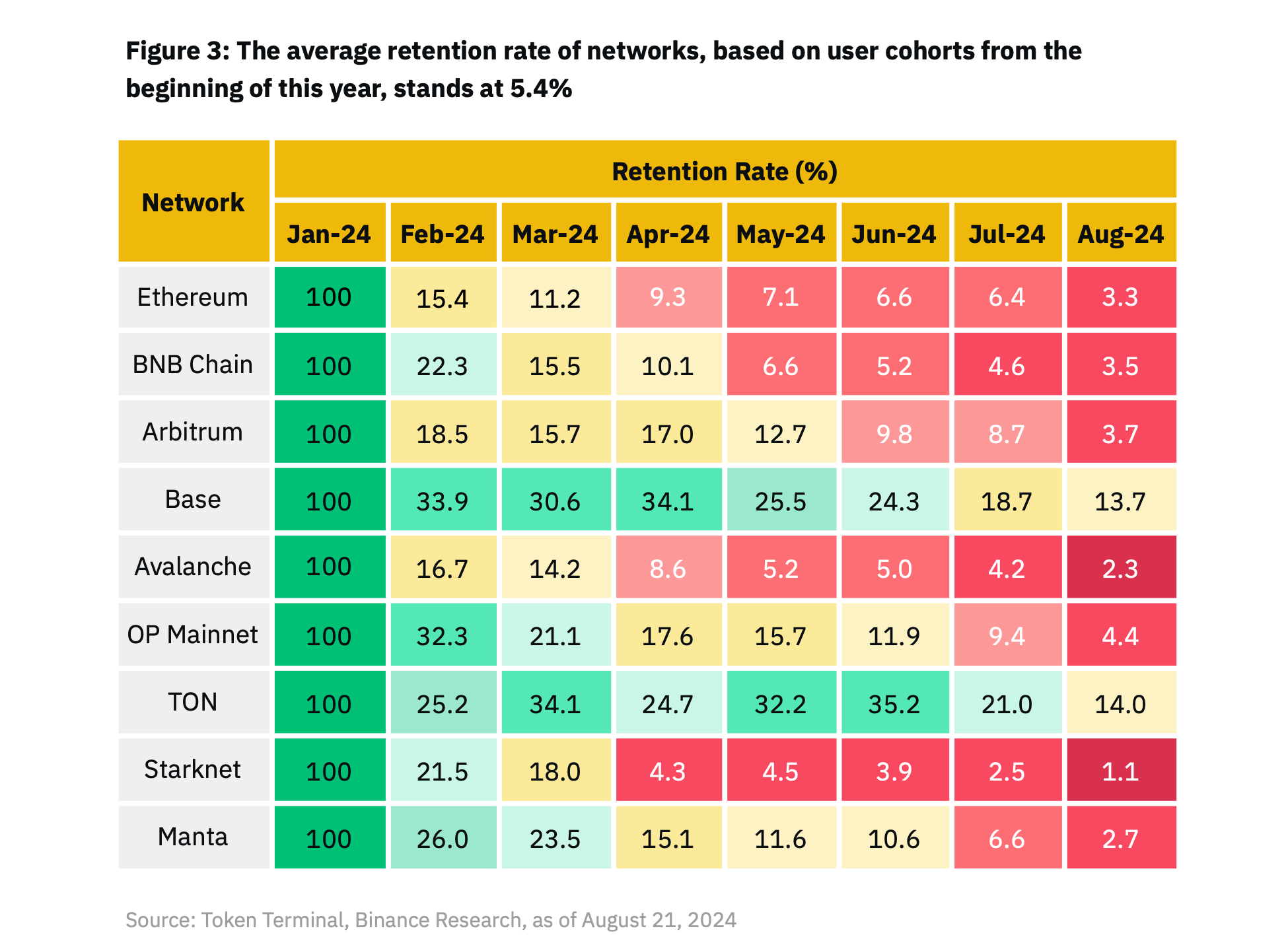

Binance Research framed this gap clearly in its 2024 Web3 adoption report: active onchain users still represent less than 1% of the global population, and the average network retention rate stands at 5.4%. The same report points to speculation and the industry’s infrastructure-heavy focus as distortions in Web3 adoption.

That does not mean Web3 lacks activity. DappRadar reported that the dapp industry reached an average of 24.6 million daily unique active wallets by the end of 2024, after a 485% increase in UAWs during the year.

The question is different: how much of that activity turns into repeat product behavior?

This is the retention question Web3 teams need to ask more often. Not “how many wallets touched the product?” but “how many users built a habit, kept capital in the system, and returned when the incentive disappeared?”

Green Dots’ internal retention research makes the same distinction: Web3’s retention problem is not that no one comes onchain. It is that many users come for a transaction, a campaign, a token, an airdrop, or a market moment — then leave because the product never becomes a recurring financial habit.

Investment products are naturally hard to retain

Fintech retention data is useful because it removes some of the crypto-specific noise.

Even outside Web3, finance apps lose users quickly. OneSignal’s 2024 mobile app benchmark data shows average app retention of 28.29% on Day 1, 17.86% on Day 7, and 7.88% on Day 30 across its dataset.

Adjust’s 2025 mobile app trends data gives a harsher benchmark for finance apps: 13% Day 1 retention, 6% Day 7 retention, and 3% Day 30 retention. AppsFlyer’s Europe finance app analysis found European investment apps dropping to 4% Day 30 retention.

The point is not to compare every benchmark 1:1. These reports use different cohorts, geographies, and definitions.

The useful pattern is simpler: investment apps are not naturally sticky.

Banking products retain better because they sit inside recurring financial life. Salary arrives there. Bills leave from there. Cards, transfers, subscriptions, and account checks bring the user back.

Investment products are more episodic. Users open them when markets move, when they have capital to deploy, or when a specific opportunity appears.

This is why trading, investing, crypto, and yield products often follow attention cycles. Usage spikes when volatility, narratives, or incentives are high. It fades when the market becomes quieter.

For Web3 apps, this matters because many products are closer to investment apps than banking apps. They ask users to take risk, understand financial mechanics, make capital decisions, and return even when the emotional reward is lower.

That is a hard retention environment by default.

What wealth and fintech data tells us about retention

Wealth management data gives a more useful lens than generic app metrics because it focuses on capital retention, not only account activity.

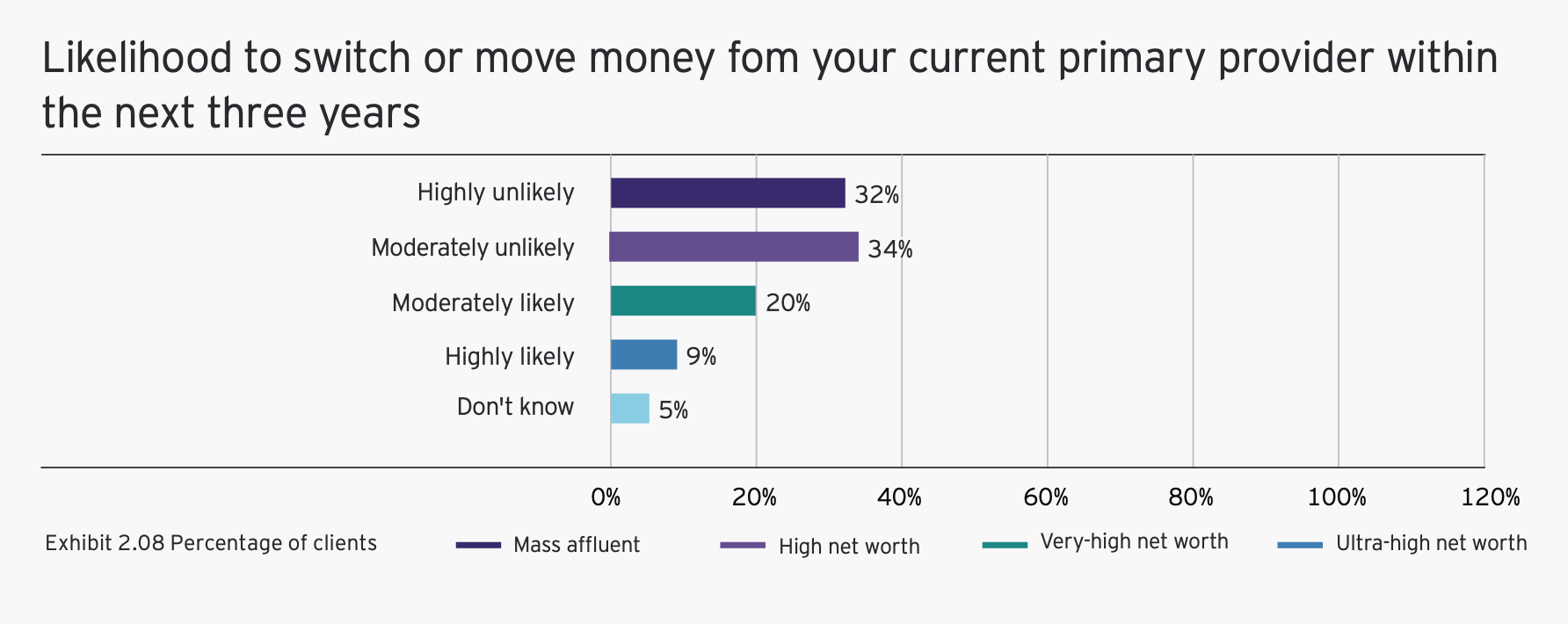

EY’s 2025 Global Wealth Research Report surveyed more than 3,500 wealthy clients across 30 markets. 29% of wealth management clients globally plan to switch their primary provider in the next three years, and historical data suggests 25–50% of a typical client’s assets may be at risk of being moved to another firm.

That second point is especially important.

A user can remain “registered” while moving most of their capital elsewhere. In Web3, a wallet can remain counted while the user’s meaningful balance, trading activity, or deposits disappear.

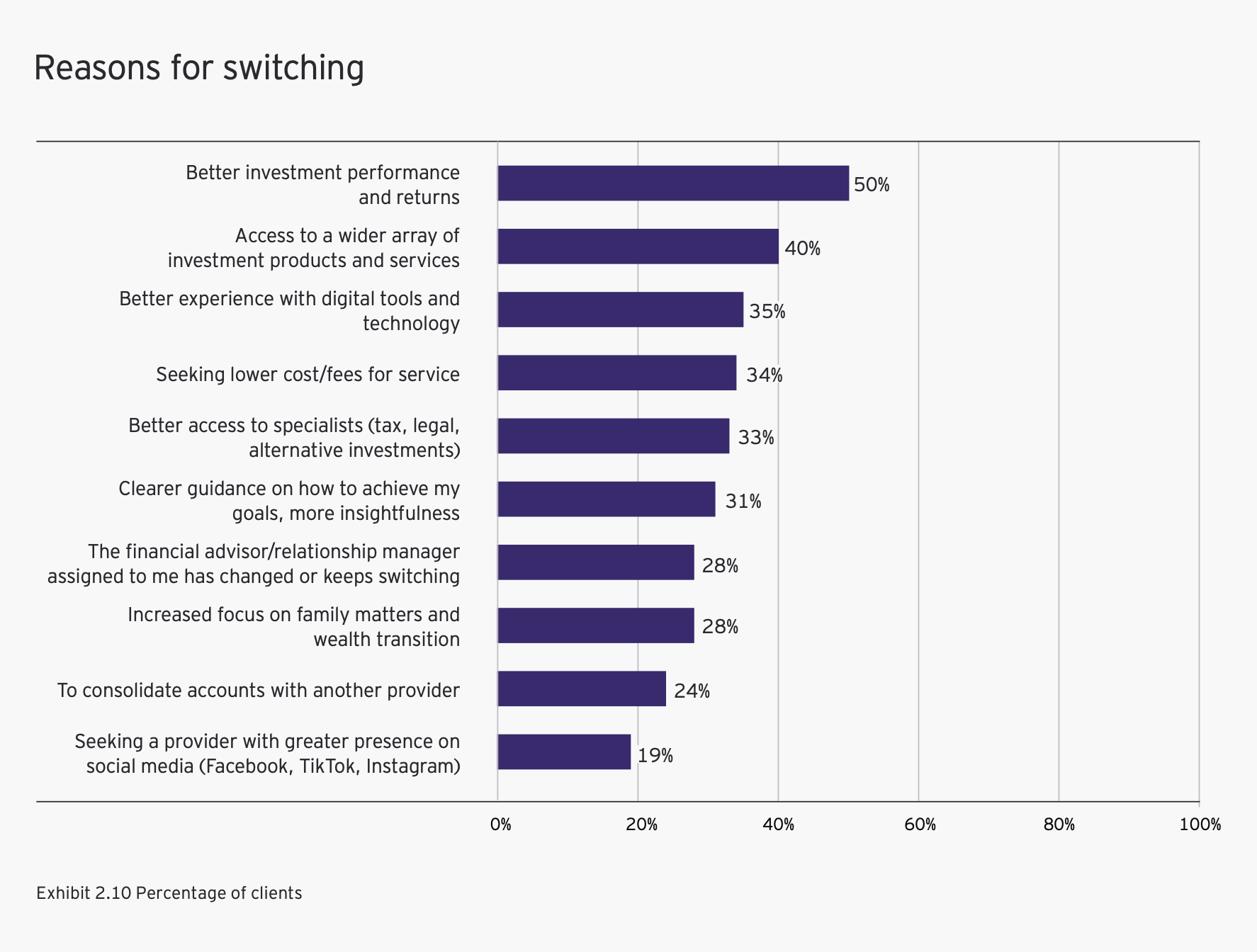

EY’s switching drivers also map well to Web3. The top reasons clients would switch wealth providers include better investment performance at 50%, better access to investment products at 40%, better digital tools at 35%, lower fees at 34%, better specialist access at 33%, and clearer goal guidance at 31%.

Translated into Web3, that means users stay when they can answer a few basic questions:

- Is the product helping me get a better outcome?

- Do I understand the risk I am taking?

- Can I access something useful here that I cannot easily access elsewhere?

- Are the tools good enough to manage my position?

- Are fees, bridges, gas, and slippage clear before I act?

- Do I trust the product when the market moves against me?

This is where many crypto products underinvest. They optimize the first action, then leave the user alone in a complex financial environment.

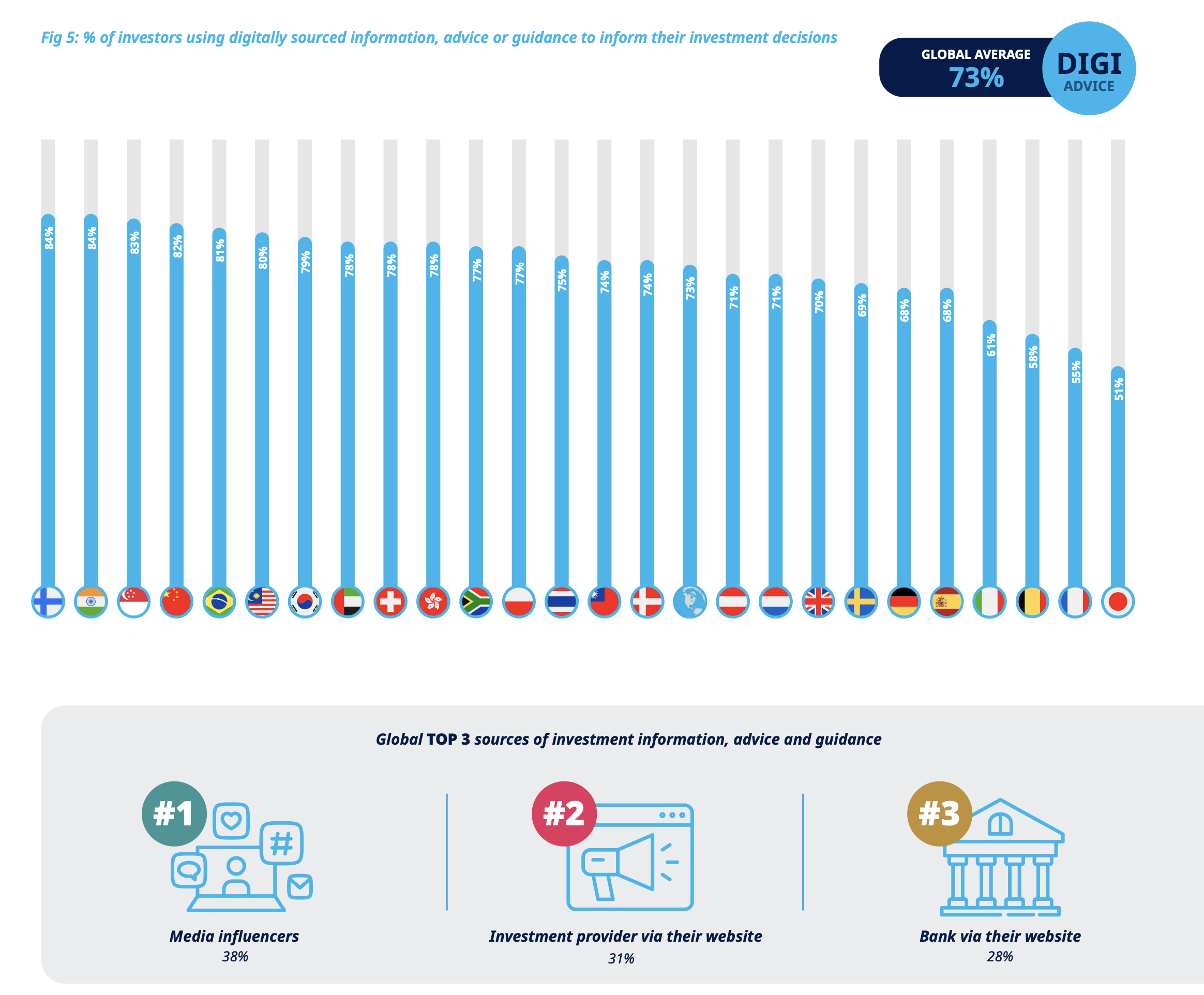

Amundi’s 2025 digital investment research adds another layer. Its report covered more than 11,000 retail investors across 25 countries and found that retail investors increasingly use digital channels for investment information and decisions. The report also found that 56% of investors who use influencers for investment decision-making have made a specific investment decision based solely on influencer information.

This is very relevant for Web3.

Users do not form conviction only inside the app. They form it through dashboards, creators, communities, Telegram groups, founder posts, research threads, exchange pages, onchain data, and other people’s explanations.

That means retention is partly a product problem and partly an information environment problem.

Why Web3 retention breaks

Most Web3 retention failures come from a few repeated patterns.

#1: Incentives attract users with weak intent

Points, quests, token rewards, and airdrop speculation can bring users into a product quickly. They can also attract people whose main job is to extract the incentive and leave.

This is not a moral failure.

It is an incentive design issue.

If the campaign rewards wallet activity more than meaningful product adoption, users will optimize for wallet activity. If the product does not create a reason to return after the reward, retention will collapse.

#2: The product does not map to a recurring financial job

A user may connect a wallet once to mint, bridge, stake, farm, claim, or trade. That does not mean the product has earned a place in their financial routine.

The stronger Web3 retention categories tend to solve recurring jobs: moving dollars, earning understandable yield, managing collateral, tracking positions, trading with better tools, accessing liquidity, protecting assets, or automating repeated actions.

Stablecoins are a good example. a16z’s 2025 State of Crypto report frames stablecoins as one of the clearest signs of crypto maturation, alongside institutional adoption and broader onchain activity. Stablecoins are retention-positive because they can sit inside repeated financial behavior: transfers, savings, payments, settlement, remittances, yield allocation, and treasury management.

The user has a reason to come back.

#3: Users do not understand the product well enough to stay

A user can be convinced by a narrative and still fail to build conviction.

This is common in DeFi, trading, and yield products. The user enters because the APY is high, the KOL explanation sounds credible, or the market is excited. Then the first drawdown, depeg scare, bridge issue, liquidation risk, or reward cut arrives.

If the user does not understand the product beyond the campaign narrative, they exit.

Education is often treated as top-of-funnel content. For financial products, it is retention infrastructure.

#4: Trust gaps compound quickly

Fintech research keeps pointing back to trust, service quality, satisfaction, and reliability as retention drivers. In Web3, trust can break in very small moments.

A failed transaction. A confusing bridge. A wallet warning. A hidden fee. A vague yield source. A dashboard that does not explain risk. A protocol response that takes too long during a crisis.

Each one teaches the user that capital may be safer somewhere else.

#5: Web3 measures vanity activity instead of retained behavior

Wallet count, TVL, campaign participants, quest completions, and social impressions are useful signals. They are not enough.

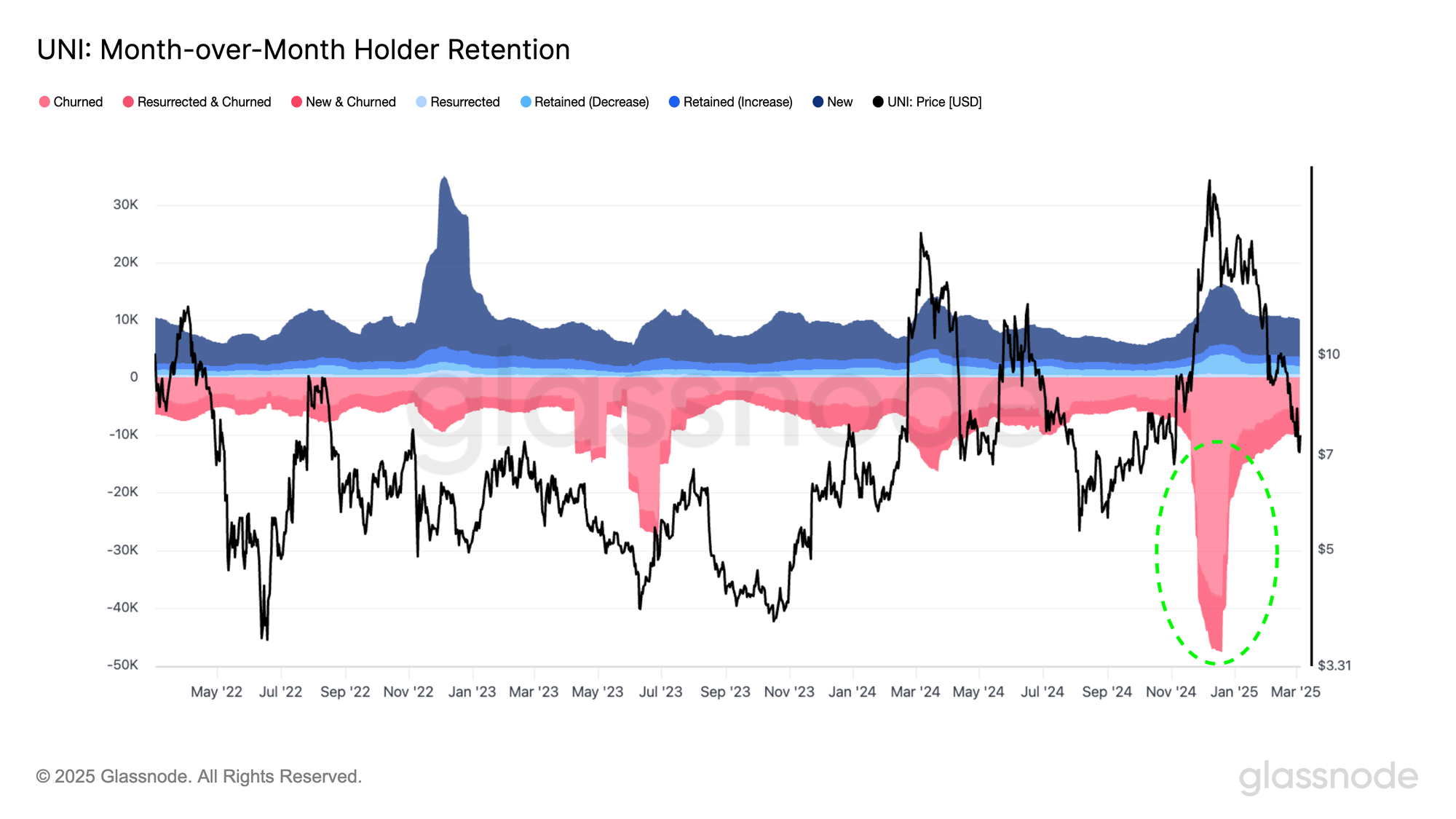

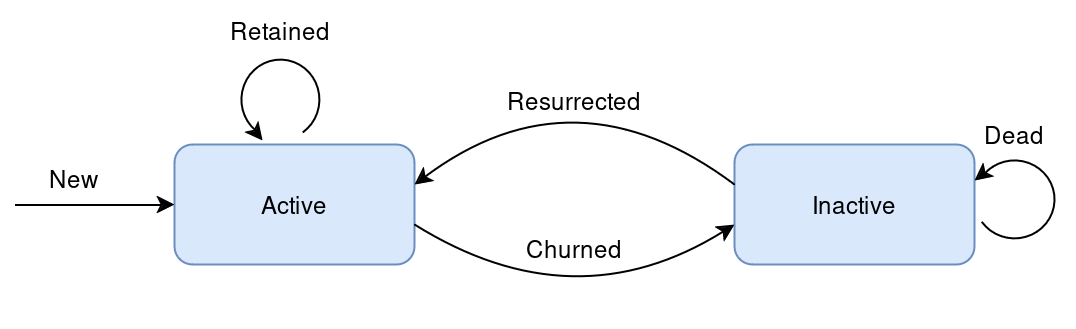

Glassnode’s 2025 onchain retention framework separates activity retention from holder retention: do addresses keep transacting, and do they keep holding the asset? Web3 teams should measure repeated behavior and sustained ownership rather than treating one-time wallet activity as proof of demand.

For apps and protocols, the better questions are:

Did the user return without a new incentive?

Did they repeat the core action?

Did they keep capital in the system?

Did their position size grow, shrink, or disappear?

Did they move from speculative action to a recurring financial routine?

The retention shift: from speculative user to recurring financial user

A useful Web3 retention framework has five stages.

1. Speculative attention

The user notices the product because of a market narrative, token campaign, KOL post, airdrop rumor, points program, launch event, or yield opportunity.

This stage is often where Web3 marketing is strongest. The market knows how to create attention.

But speculative attention is unstable. It does not mean the user understands the product, trusts the product, or intends to return.

2. First useful transaction

The user completes a first action that creates personal relevance.

This could be a trade, deposit, swap, bridge, collateral action, subscription, portfolio setup, vault entry, or stablecoin transfer. The key word is useful. If the user only performs an action to qualify for a reward, the product has not yet proven much.

The first transaction should answer: “Why would I use this again?”

3. Trust formation

The user begins to believe the product is safe enough, clear enough, and valuable enough to revisit.

Trust formation depends on UX, risk communication, product reliability, social proof, transparent metrics, founder communication, creator explanations, and how the team behaves when something goes wrong.

In one early-stage trading terminal product, our CustDev research into retention factors before a major marketing push helped identify onboarding and stickiness gaps: where users lost confidence, which workflows felt unclear, and which product moments made the terminal feel useful enough to revisit.

The point was not to “market harder.” It was to understand what needed to become clearer before acquisition scaled.

4. Recurring financial behavior

The user comes back because the product now has a job in their financial life.

They check positions. Rebalance. Trade. Move stablecoins. Monitor risk. Claim yield. Adjust collateral. Follow signals. Export data. Track performance. Use automation. Return because the product reduces effort or improves a decision.

This is where retention starts to look like habit.

5. Capital retention

The user keeps meaningful capital inside the system.

This is the highest-value retention layer for DeFi, trading, yield, wallets, and fintech-adjacent crypto products. It is also the layer most teams under-measure.

A wallet can return with no capital. A user can hold a tiny balance for airdrop eligibility. A product can show account retention while losing share of wallet.

Capital retention is the stronger signal.

What our internal DeFi retention research shows

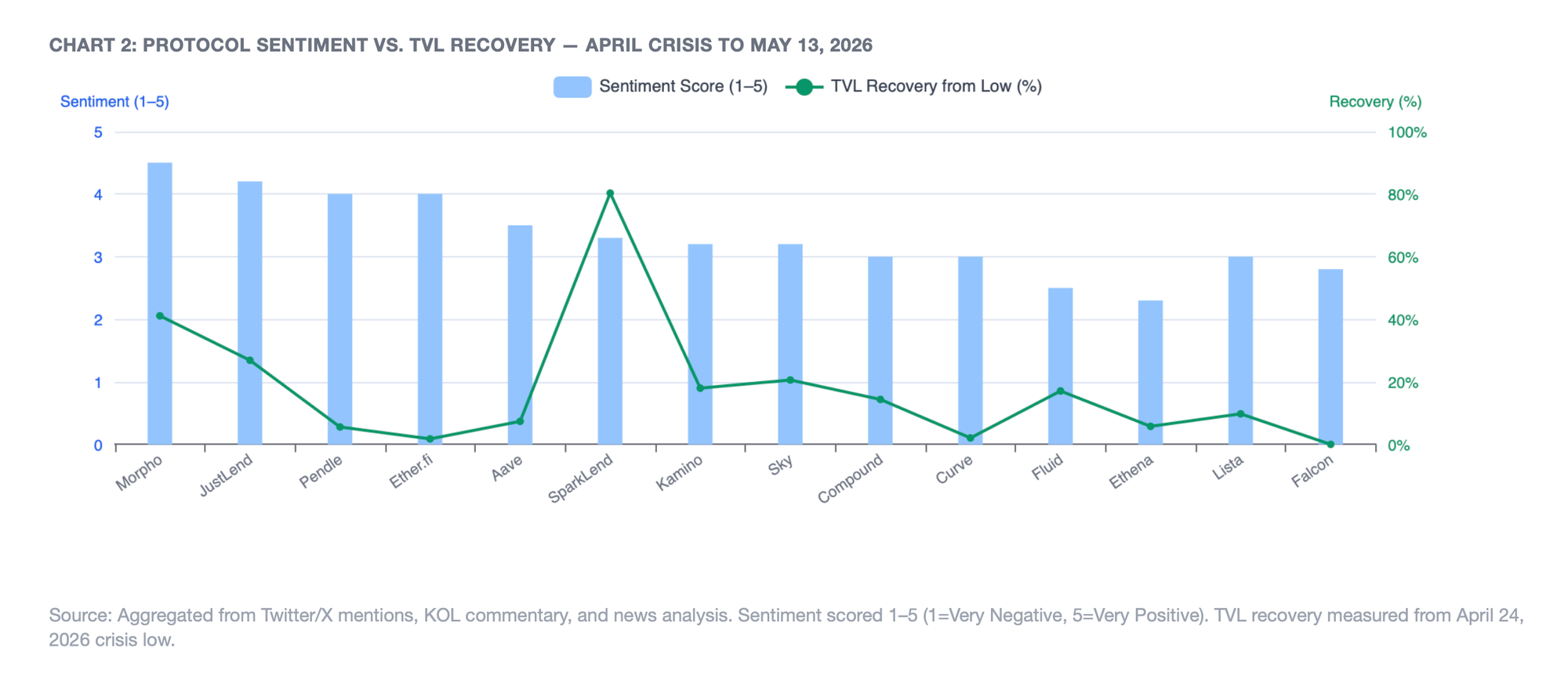

In May 2026, we analyzed 14 yield-focused DeFi protocols across major crisis events between October 2025 and May 2026.

The study’s core finding is useful beyond DeFi: protocols with higher retention through stress shared three patterns — isolated or modular risk architecture, rapid and transparent governance responses within 24–48 hours, and user bases not overly concentrated in yield-farming capital.

That is a retention lesson, not only an investment lesson.

During quiet markets, many products can appear healthy. Incentives and rising prices hide weak user conviction. Stress reveals who is actually retained.

The study also found clear differences across protocols. Morpho Blue, Sky Lending, and JustLend showed stronger TVL stability or recovery than protocols with more fragile capital bases or direct crisis exposure. In fact, user retention through crisis is one of the strongest indicators of protocol health because it separates durable product-market fit from incentive-inflated TVL.

For builders, the implication is direct.

Retention is not measured only during growth campaigns. It is measured when the product is less exciting, the yield is lower, the market is stressed, and users have alternatives.

How Web3 apps can improve retention

Web3 teams do not need to copy fintech products directly. Crypto has different mechanics, different users, different risks, and different distribution channels.

But the retention logic is similar.

Build around recurring jobs, not campaign moments

The core product should answer a repeated user need.

For a trading terminal, that might be better execution, faster discovery, risk alerts, portfolio tracking, or decision support.

For a DeFi protocol, it might be stable yield, credit access, collateral management, or treasury allocation.

For a wallet, it might be safer storage, recurring payments, identity, rewards management, or easier access to apps.

A campaign can introduce the product.

It cannot create the recurring job by itself.

Design the post-incentive path before launching incentives

Before running a points campaign or airdrop, teams should define what the user is supposed to do after the incentive.

What is the second action?

What is the third action?

What should happen after the reward is claimed?

What product feature makes the user return next week?

What cohort should retain better than farmers?

If those answers are vague, the campaign will likely generate activity that decays.

Make performance and risk easier to understand

Financial users stay when they understand what is happening to their capital.

For Web3 products, this means clearer performance dashboards, risk labels, benchmark comparisons, fee explanations, scenario examples, and plain-language product education.

Yield products should explain where yield comes from. Trading tools should explain what advantage the tool gives. DeFi apps should make liquidation, bridge, oracle, counterparty, and smart contract risks easier to understand.

Reduce friction where it damages trust

Not all friction is bad. Some friction protects users.

But confusing friction damages retention: failed transactions, fragmented signing flows, slow confirmations, missing position data, poor mobile support, weak recovery paths, and dashboards that require users to calculate risk manually.

Every confusing moment increases the chance that the user decides the product is not worth the effort.

Treat education as retention infrastructure

Most Web3 education is built for awareness.

Good retention education should help the user stay.

That means explaining how to use the product after first action, what to monitor, how to think about risk, what good usage looks like, and what signals should make the user adjust behavior.

Creators can help here, but the product team needs to own the source material. Otherwise, the narrative lives outside the product and can move against it.

Measure cohorts by behavior and capital

Web3 teams should look beyond aggregate wallet activity.

Useful retention metrics include:

- repeat core action rate;

- post-incentive return rate;

- capital retained by cohort;

- average balance or position size by cohort;

- share of users who complete a second and third meaningful action;

- dormant capital versus active capital;

- churn after reward changes;

- retained users by acquisition source;

- retention during market stress.

For DeFi and investment-style products, the most important question is often not “how many users came back?” It is “how much relevant capital stayed, and why?”

KOLs can create the first action, but they cannot retain users alone

KOL marketing matters in Web3 because creators can transfer trust faster than brand channels.

A good creator can explain a complex product, put it into market context, compare it with alternatives, and make the first action feel credible. This is why KOLs remain an important part of Web3 user acquisition and launch strategy.

But KOLs cannot carry retention alone.

Amundi’s digital investment research shows that many retail investors already use influencers and expert media as part of investment decision-making. In Web3, this pattern is even more visible because creators often act as translators between technical products and market participants.

The risk is that narrative-led acquisition can outpace product-led retention.

A user may enter because a creator made the opportunity understandable. They will stay only if the product keeps proving itself after that first action.

We normally treat KOL campaigns as a distribution layer, not a standalone growth engine – and advise our clients to optimise for long-term KOL relationships.

Creator campaigns work best when they are connected to onboarding, education, community follow-up, and a real post-campaign retention path.

The next Web3 winners will retain behavior, capital, and trust

The market has spent years improving speculative acquisition. But the next stage of Web3 growth will be less forgiving.

Teams will need to show that users return after the incentive, understand the product beyond the narrative, trust the experience during stress, and keep meaningful capital in the system.

Fintech data gives the direction. Investment products retain when users trust them, understand the outcome, access useful tools, receive clear guidance, and integrate the product into recurring financial routines.

For Web3, the same principle applies with higher stakes.

The goal is not to acquire the most wallets during a campaign window. The goal is to turn speculative attention into repeated behavior, and repeated behavior into retained capital and trust.

That is the harder growth problem. It is also the one that will matter more.

Subscribe to get new field notes, studies, and frameworks from Green Dots Research when they go live.

Author note

Written by Stacy Muur, founder of Green Dots. Green Dots works with Web3 teams on GTM strategy, creator-led distribution, founder growth, and launch architecture.