What Web3 Neobanks Teach Us About Consumer GTM

Web3 neobanks are not winning through better cards alone. Our research found that the strongest GTM systems combine payment trust, referral design, creator-led distribution, public proof, and activation into repeated usage.

We analyzed nine Web3 neobank platforms to understand how this category is actually reaching users.

The category looks simple from the outside: crypto cards, stablecoin balances, cashback, yield, and access to everyday payments. But the GTM work underneath is much harder.

A Web3 neobank has to solve several problems at once.

- It needs trust, because users are moving money.

- It needs utility, because a card that does not become part of daily spending quickly becomes a novelty.

- It needs distribution, because consumer finance is expensive to scale.

- And it needs activation, because account creation alone does not mean the product is working.

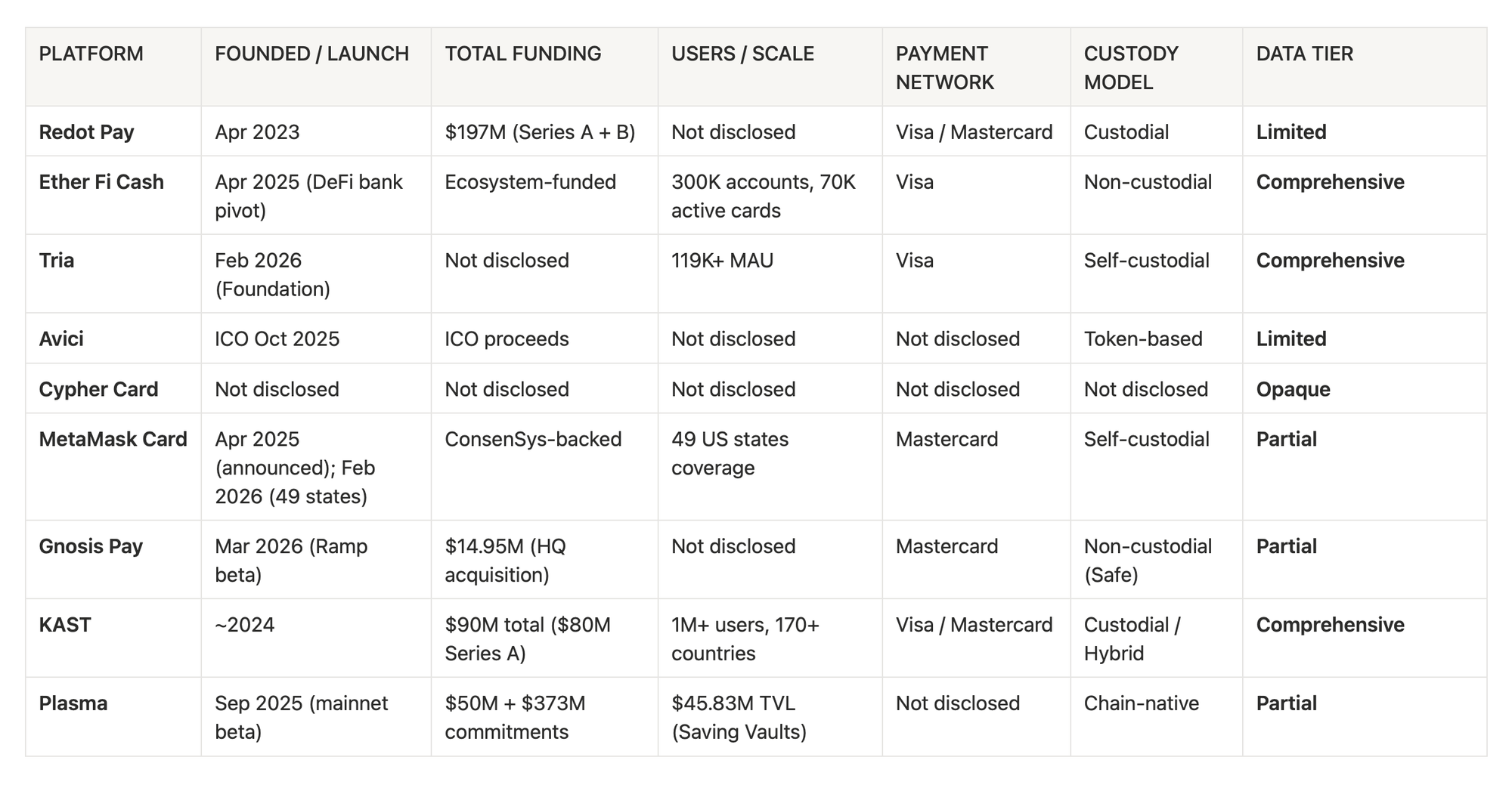

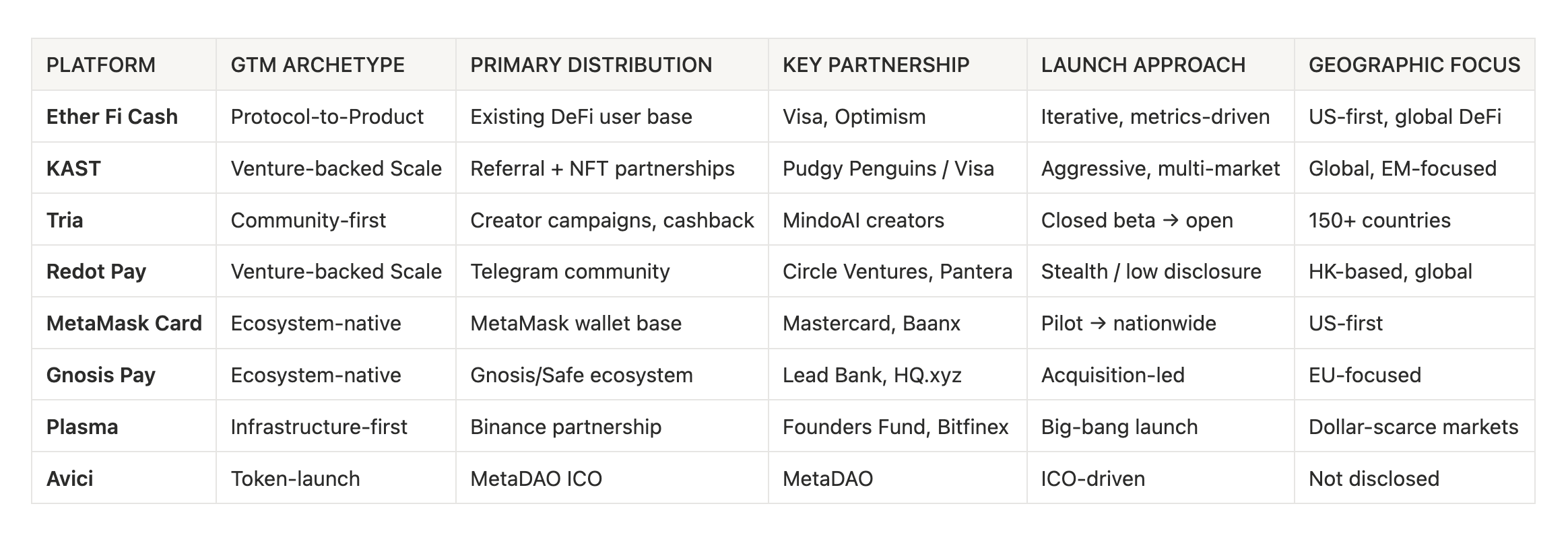

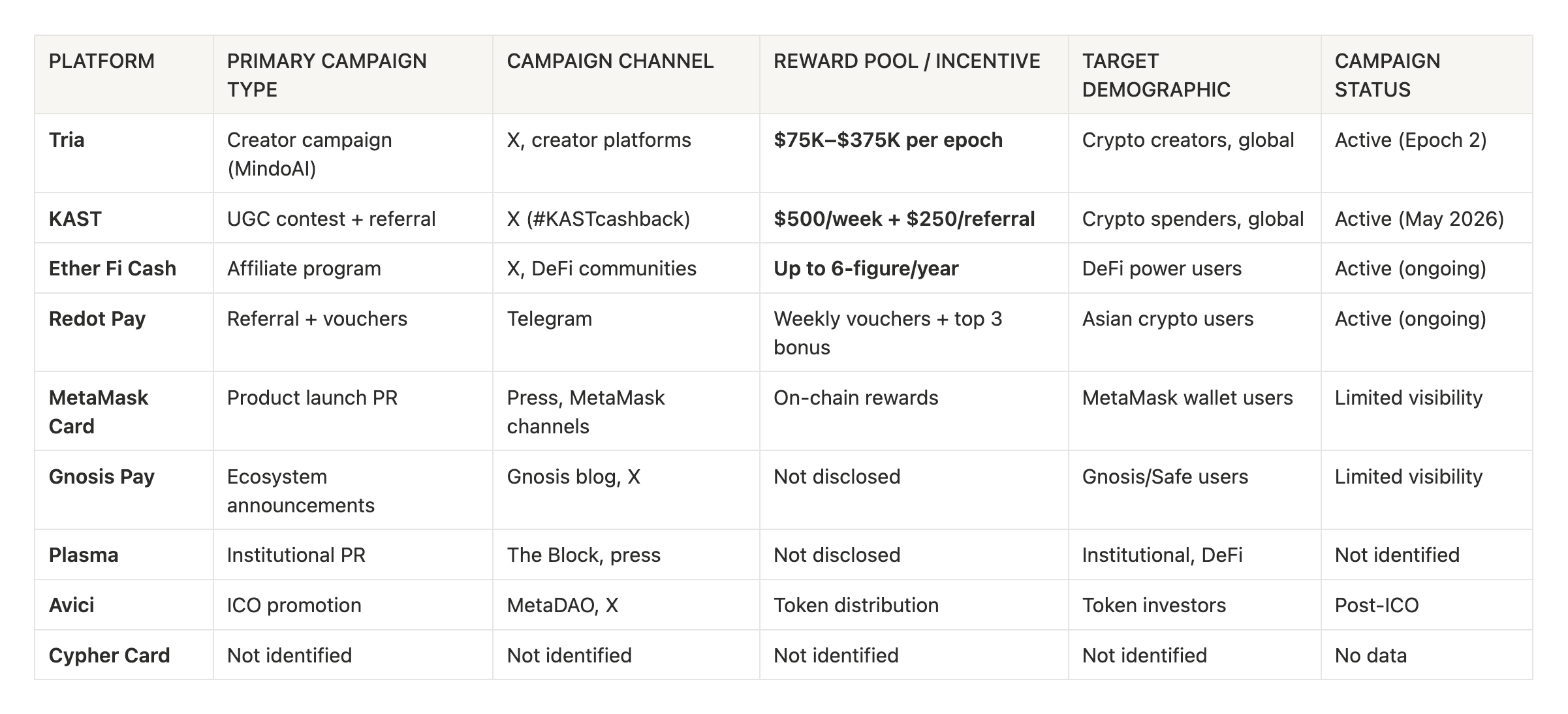

In this internal Green Dots research, we looked at nine platforms: KAST, Ether Fi Cash, Tria, MetaMask Card, Gnosis Pay, Plasma, Redot Pay, Avici, and Cypher Card. The data was based on publicly available information as of May 2026, including platform announcements, public metrics, media coverage, DeFiLlama, X, and industry sources.

Green Dots Research is the hub where we collect the most insightful pieces and studies on building successful Web3 products.

Subscribe to get new studies in your inbox.

The category has already split into clear GTM tiers

We discovered a clear separation between scale leaders and platforms with limited public traction data.

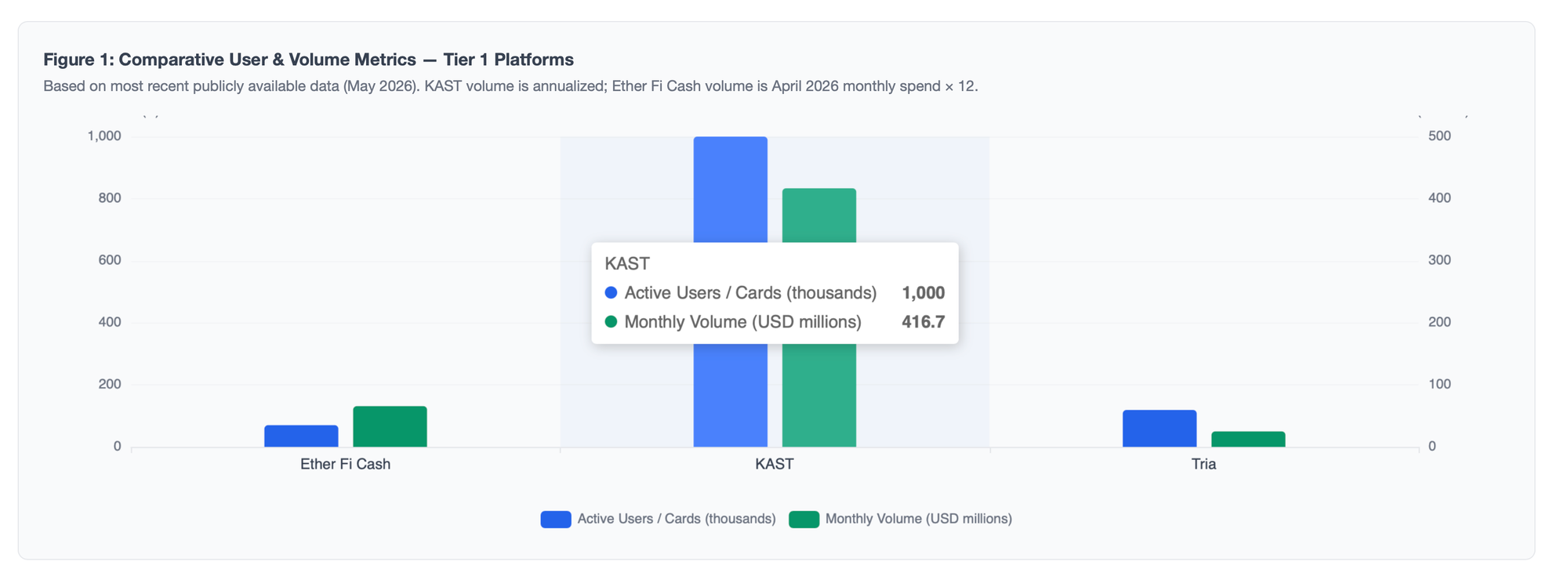

The strongest public GTM signals came from KAST, Ether Fi Cash, Redot Pay, and Tria.

- KAST stood out for scale: 1M+ users across 170+ countries and an estimated $5B in annualized transaction volume.

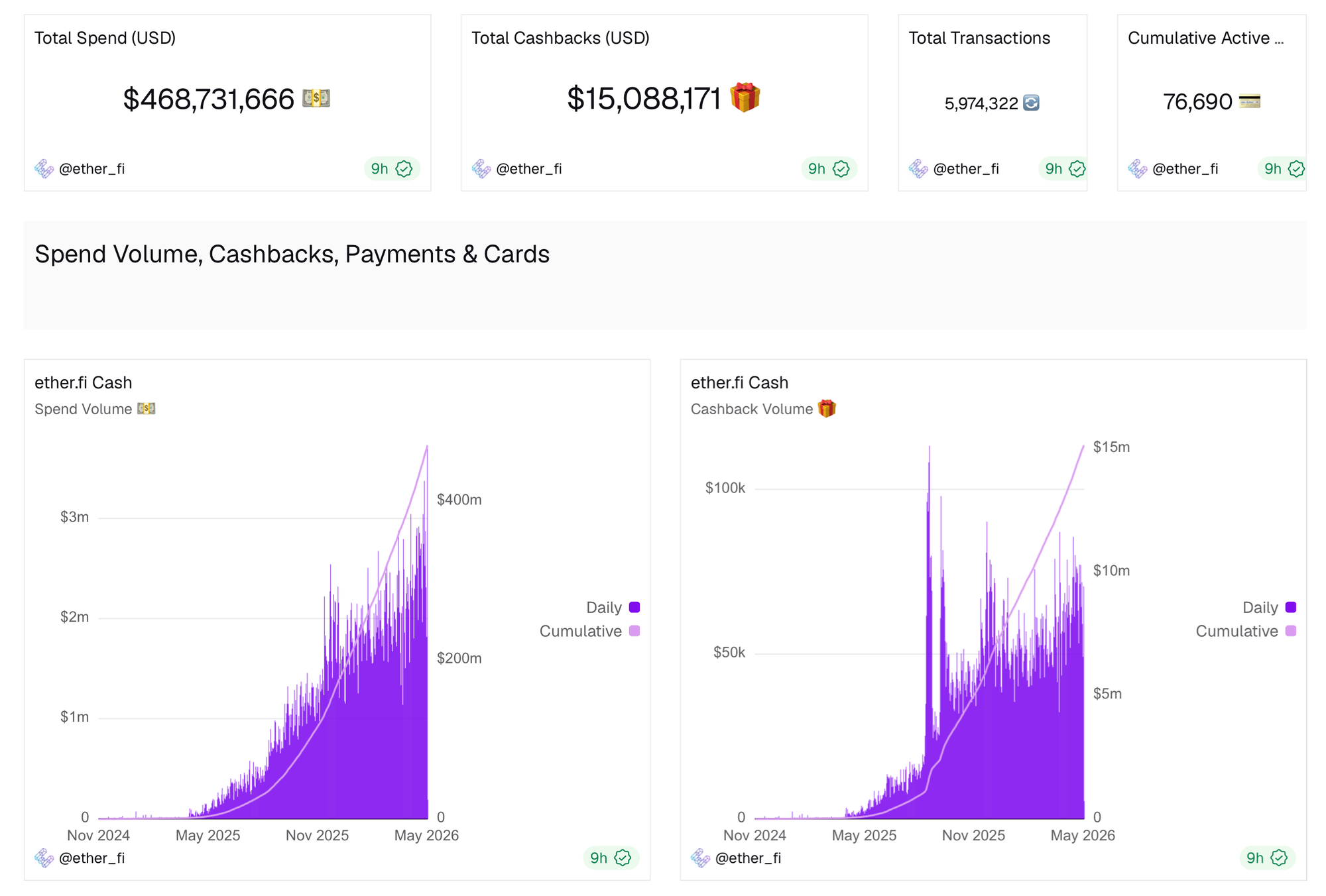

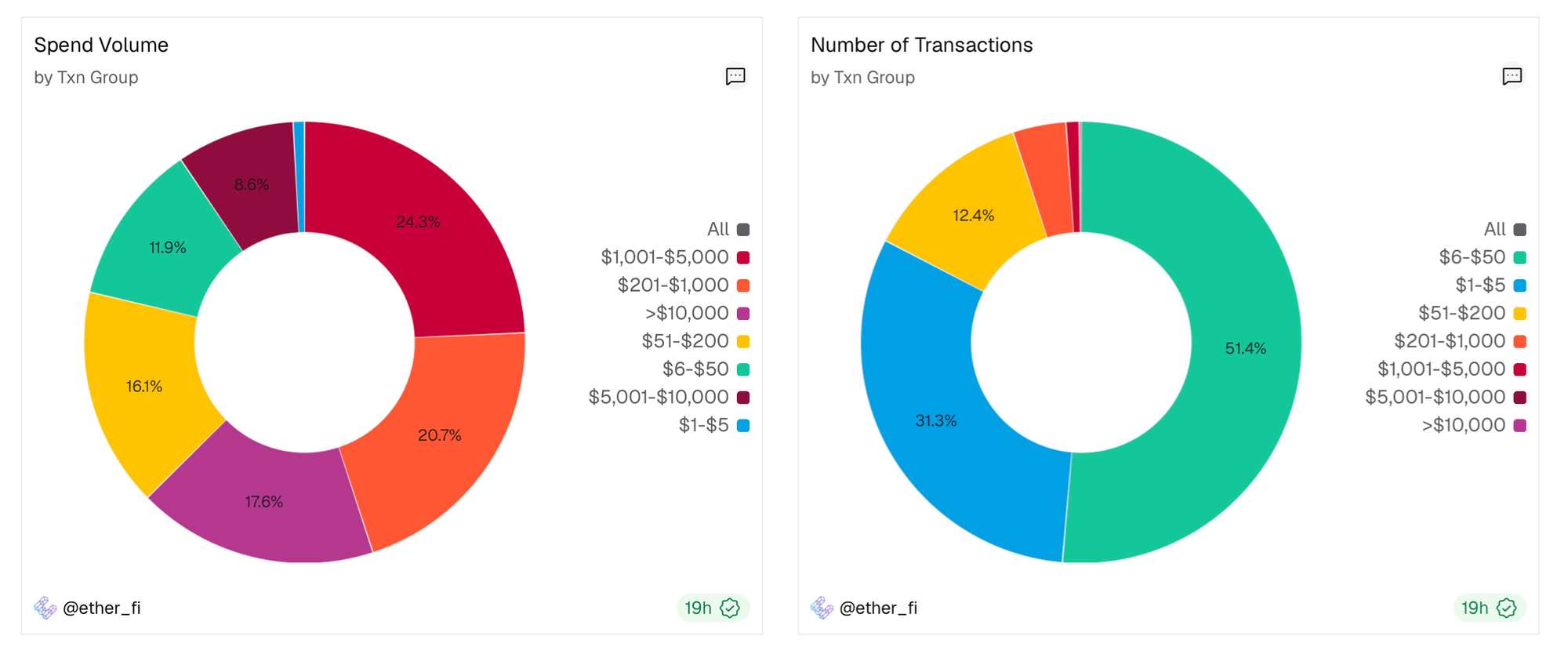

- Ether Fi Cash stood out for transparency and spend depth, with 300K accounts, 70K active cards, and $65.7M in monthly card spend reported for April 2026.

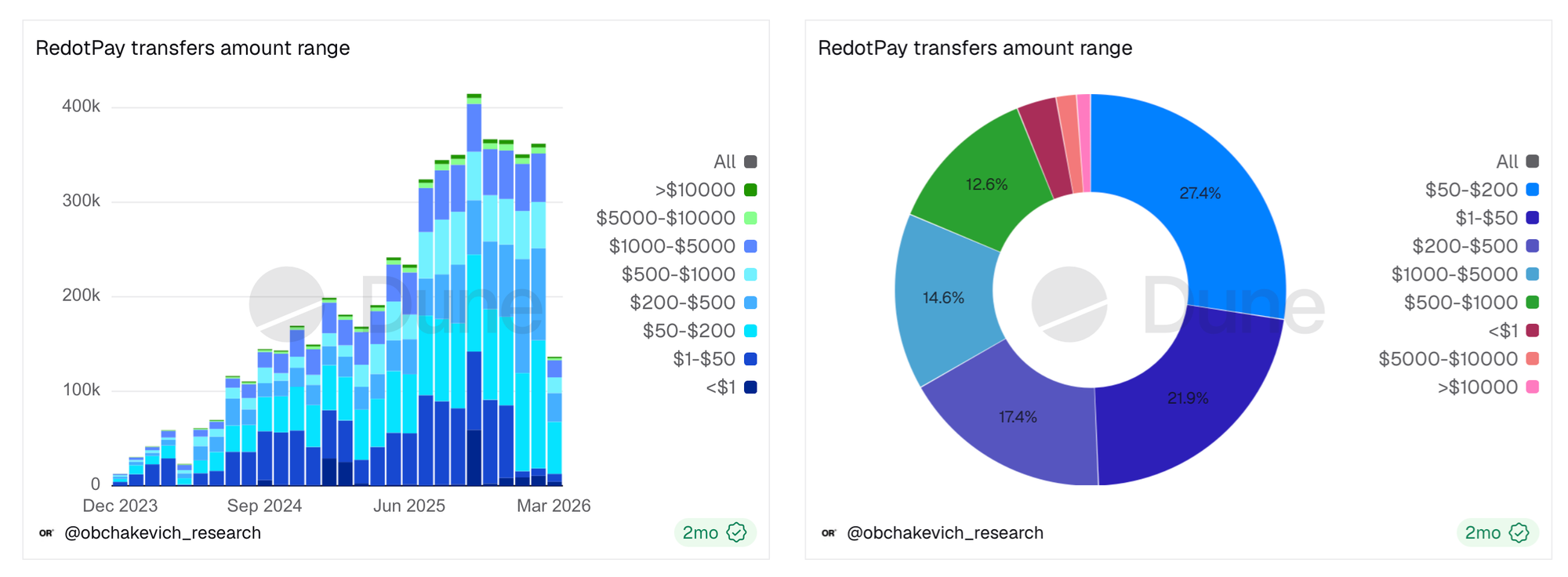

- Redot Pay stood out for its traction in emerging markets, with ~$300M in monthly card transaction volume.

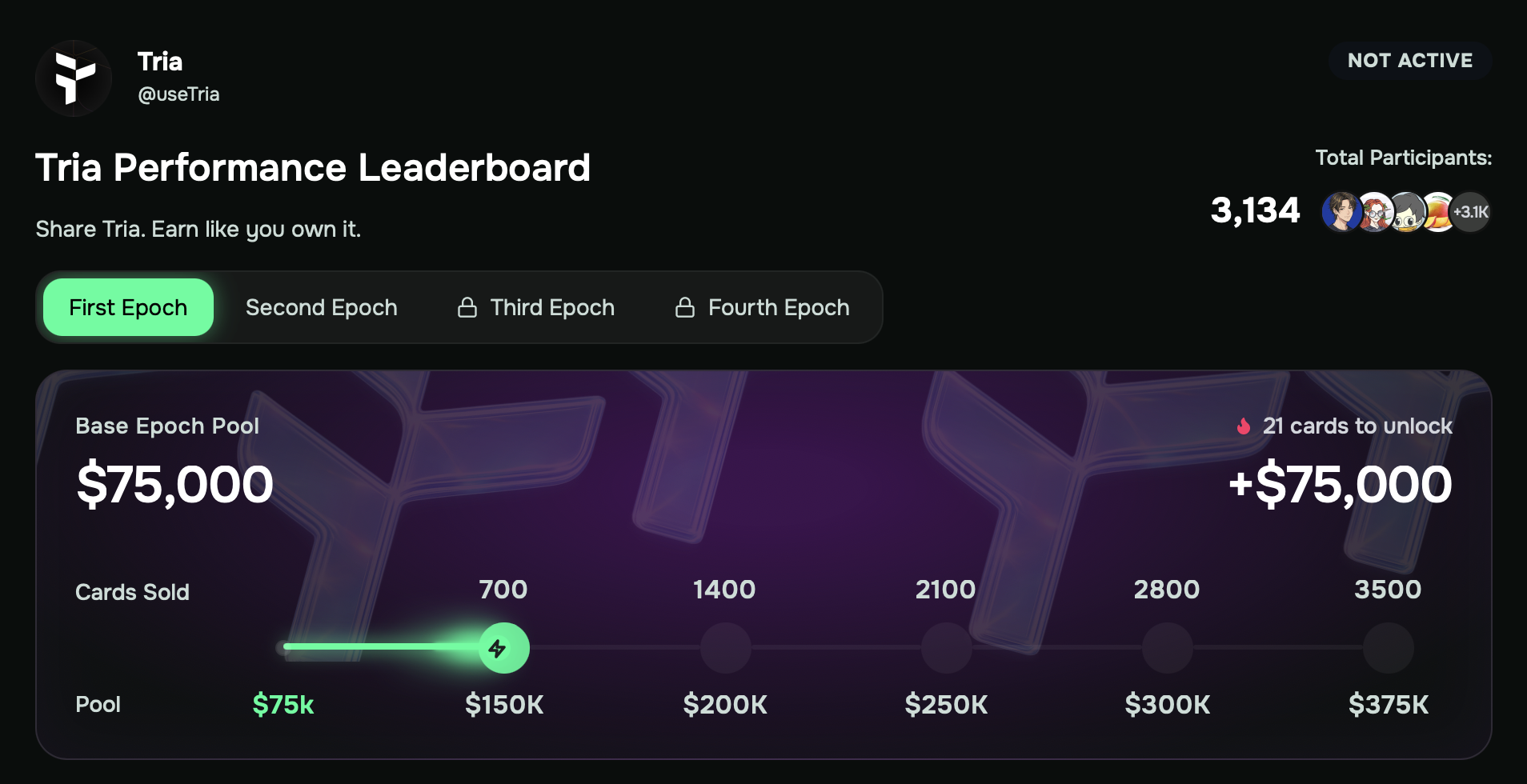

- Tria stood out for speed, reporting 119K+ monthly active users and $100M+ processed volume during a four-month closed beta period.

The rest of the market is harder to read.

Some platforms have strong institutional backing or ecosystem advantages, such as MetaMask Card, Gnosis Pay, and Plasma. But public user metrics are either partial, TVL-focused, or missing. That matters because in crypto, transparency itself becomes part of the GTM.

When a platform publishes usage, spend, cashback, or active card numbers, it gives the market something to repeat. The metric becomes content. The content becomes social proof. The social proof reduces perceived risk for the next user.

Web3 neobank GTM has four main archetypes

Across the nine platforms, we saw four GTM patterns.

The first is the protocol-to-product pivot. Ether Fi Cash is the clearest example. It started with an existing DeFi user base and expanded into a consumer-facing card product. The advantage is obvious: the audience already has on-chain assets, understands yield, and has a reason to use a spending product that connects to DeFi.

The challenge is activation. DeFi users may open accounts because the product is interesting, but that does not mean they will use the card every week.

The second is the venture-backed scale play. KAST and Redot Pay fit here. These companies raise significant capital, build broad market coverage, and push aggressively into geography, partnerships, and acquisition.

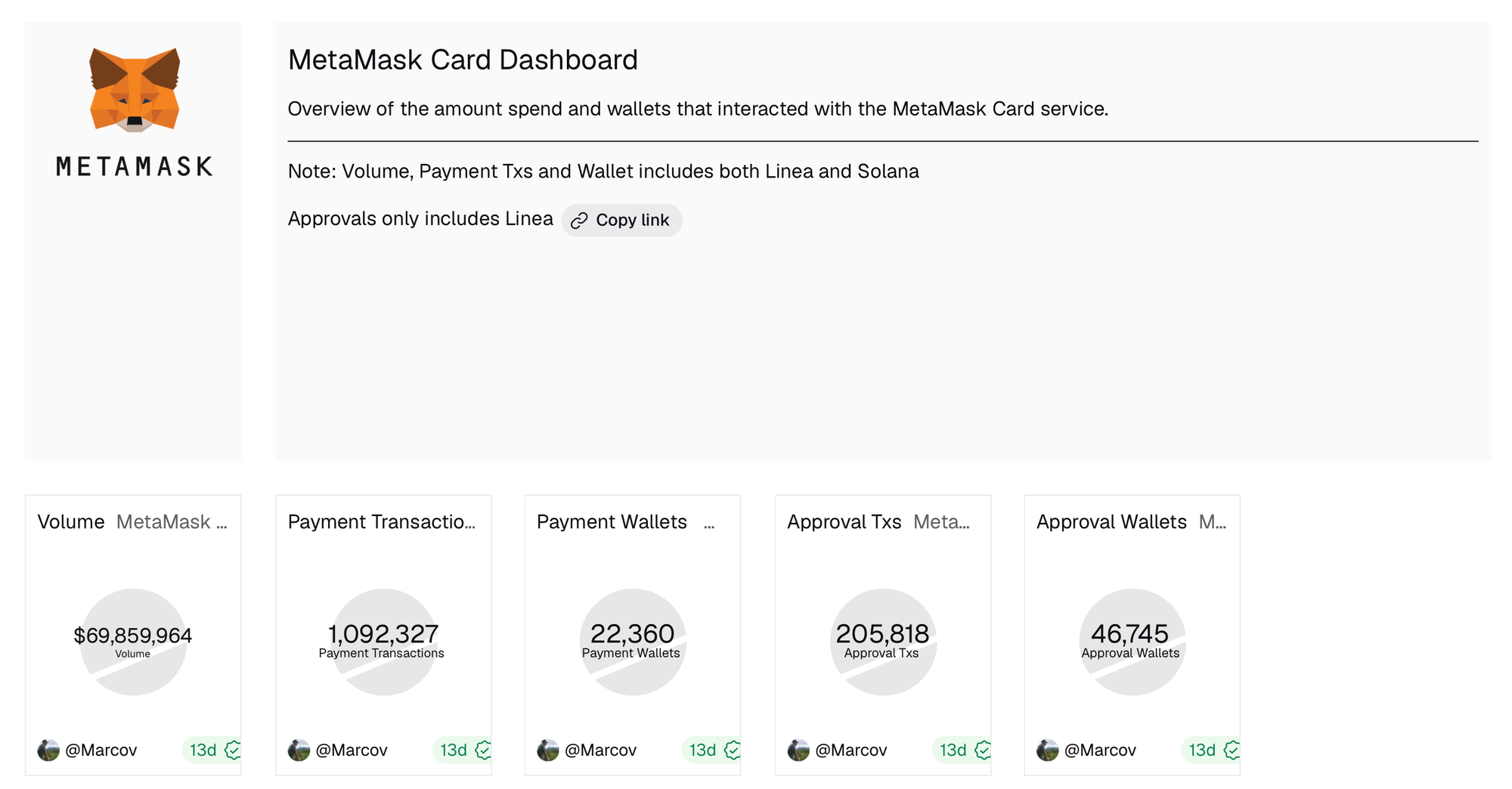

The third is ecosystem-native distribution. MetaMask Card and Gnosis Pay are built on top of existing infrastructure and user bases. MetaMask has the clearest distribution advantage because of its large wallet user base. But the hard part is conversion. A wallet user is not automatically a card user.

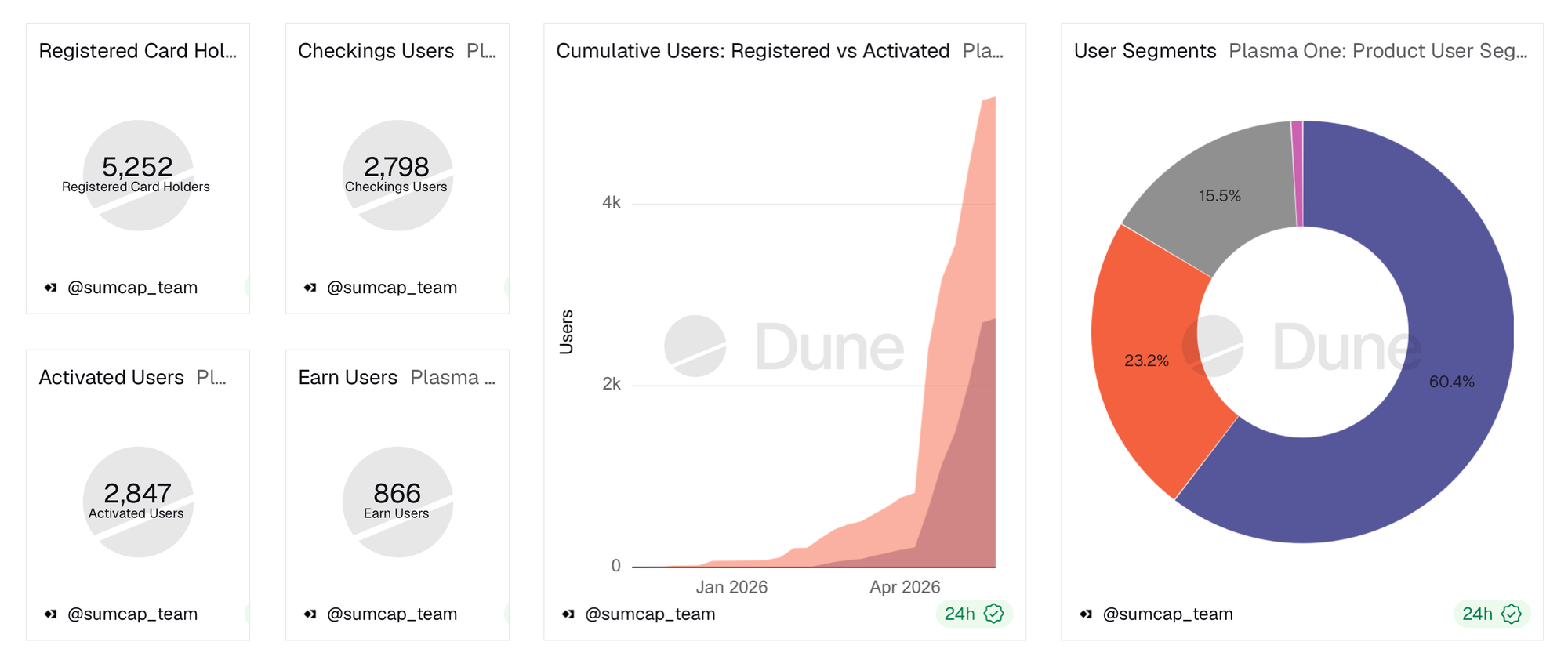

The fourth is infrastructure-first GTM. Plasma represents this pattern. It starts with stablecoin infrastructure, chain-native products, and institutional partnerships, then moves toward consumer products. This can create stronger long-term control, but it usually has a slower consumer activation path.

The winners have a real reason for users to switch

A card alone is not enough.

The better-performing Web3 neobanks give users a reason to change financial behavior. That reason usually comes from one of three places: yield, cashback, or better access to stablecoin payments.

- KAST offers high cashback and stablecoin yield positioning.

- Ether Fi Cash connects spending to DeFi-native capital.

- Tria uses cashback and token incentives to create early user momentum.

These mechanics matter because consumer finance products rarely win through interface alone.

A user does not switch spending behavior because a product sounds interesting. They switch when the product gives them a clear economic reason, a trust reason, or a convenience reason.

The strongest Web3 neobank products combine at least two of those.

For consumer founders, this is the key question: what is the real switch trigger?

It cannot be “better UX” in the abstract. It has to be specific. More yield. Better access. Lower friction. Better rewards. Local currency protection. Stronger status signal. Better community belonging. More useful money movement.

Without that switch trigger, marketing has to carry too much weight.

Payment network partnerships are trust infrastructure

Every scaled Web3 neobank in the research had a serious payment network story.

KAST works with Visa and Mastercard rails. Ether Fi Cash uses Visa. Tria uses Visa. MetaMask Card uses Mastercard. Gnosis Pay uses Mastercard infrastructure. Platforms without clear payment network partnerships had weaker public evidence of consumer-facing adoption.

This matters because payment partnerships do more than enable merchant acceptance. They reduce trust friction.

For a normal user, “crypto card” can sound risky. Visa or Mastercard acceptance changes the frame. It signals that the product is not only a crypto experiment. It can operate inside existing payment behavior.

This is insane.

— DeFi Warhol (@Defi_Warhol) April 7, 2026

Visa accounts for 96% of the total volume of crypto cards. Mastercard's share has been in a steady decline since 2025.

It's fair to say Visa has officially won the neobank battle. pic.twitter.com/BzUiSUfeeu

The broader lesson applies to any consumer product in a trust-heavy category. Distribution is easier when the product borrows legitimacy from infrastructure the user already understands.

Referrals are the primary acquisition engine

We did not see strong evidence that traditional paid advertising is the main growth channel for Web3 neobanks.

Instead, the strongest acquisition mechanics were referral programs, creator campaigns, cashback-sharing contests, and community-driven incentives.

KAST has one of the most interesting referral designs in the group. Its rewards are tied to spending behavior, not just account creation. A referred user must spend to trigger meaningful rewards. That makes the referral program much more useful because it filters for higher-quality users.

Tria uses a different structure. Its cashback distributions, creator campaigns, and TRIA token incentives create a loop where users and creators both have reasons to talk about the product.

Ether Fi Cash uses an affiliate model that can reward promoters over time, based on ongoing card spend rather than a one-time signup.

This is where many consumer teams make a mistake.

They treat referrals as a growth hack. In practice, a strong referral system is product design, financial modeling, and distribution strategy at the same time.

The best referral programs answer four questions:

What user behavior proves quality?

When should the referrer be rewarded?

How do we prevent low-intent users from gaming the system?

KAST’s spend-linked referral structure is strong because it does not reward empty signups. It rewards behavior closer to the business model.

That is the standard more consumer products should use.

Creator campaigns work better when they are tied to behavior

Tria’s creator campaign is one of the more useful examples in our report.

Instead of running a broad influencer campaign focused only on impressions, Tria structured creator incentives around card sales and reward pools. The campaign used epochs, reward scaling, and a defined creator cohort. That matters because it moves creator marketing closer to performance marketing without reducing creators to ad slots.

Our read: this is where creator-led distribution is heading for consumer products.

The early version of creator marketing was simple: pay people with audiences to post. The better version connects creators to specific user behaviors: activation, card spend, referrals, account funding, first transaction, or repeat usage.

If the main goal is activation, this is a strong playbook.

Classic creator campaigns (pay for reach) are still useful for awareness. But in a crowded consumer category, awareness without activation is not enough. The campaign needs to create trust, explain the product, and move the user toward a real action. This is where "pay for result" works extremely well.

UGC works because financial products need proof

KAST and Tria both use user-generated content around cashback.

This may look simple, but it is strategically important. A cashback receipt is not just a post. It is a proof asset. It shows that the product works, users are getting rewarded, and the experience is not theoretical.

For Web3 products, this type of proof is valuable because users are skeptical of paid claims. A brand saying “earn cashback” is weaker than dozens of users showing actual cashback events.

Win up to $500 every week 🤑

— KAST (@KASTxyz) May 15, 2026

How to participate:

🤳 Post cashback/referral rewards

☑️ Use the hashtag #KASTcashback

🤞 Enter for a chance to win

Best post gets $500. 5 runners up get $100 each.

Share your best post now. pic.twitter.com/wIXiRcMMT9

The same logic applies outside crypto.

Geographic depth beats shallow global coverage

Many Web3 neobanks claim global reach. That sounds strong in a deck, but it does not always mean strong GTM.

KAST’s strategy is more interesting because it goes deeper into specific local payment contexts. Its Colombian Peso support through ACH and Bre-B rails shows a more serious approach to local market adoption. The same applies to its focus on Brazil and the Middle East, where stablecoin usage can connect to real currency, savings, and cross-border payment needs.

This is an important lesson for consumer founders. “Available everywhere” is not the same as “adopted somewhere.”

A product can technically serve many countries and still have no clear market wedge. Local currency support, payment rails, creator networks, regulations, community behavior, and financial pain points all shape adoption.

For neobank-like products, the best market is not always the largest market. It is the market where the product’s value proposition is most obvious.

Earlier this month, we posted a study on the stablecoin adoption in LATAM. This is a highly relevant read in the context of local marketing.

Activation is the real bottleneck

The most useful number in the report may be Ether Fi Cash’s active card ratio.

Ether Fi Cash had 300K accounts and 70K active cards, which implies that a meaningful share of users created accounts without becoming active spenders. That is not a weakness unique to Ether Fi. It is a category problem. Account creation is easy to incentivize. Spending behavior is harder.

For Web3 neobanks, the core behavior is not opening an account. It is funding the account, activating the card, making the first transaction, and returning to spend again.

For other consumer products, the same principle applies. The core behavior may be first purchase, first transfer, first saved item, first invite, first booking, first post, or first repeat session.

GTM should be built around that behavior.

Let's summarise

Web3 neobank GTM is not a channel problem.

The strongest platforms combine five things:

- A clear financial reason to switch

- Payment infrastructure that creates trust

- Referral incentives tied to valuable behavior

- Creator and UGC systems that create public proof

- Market focus deep enough to match local user needs

The weaker platforms are not always weak products. In some cases, they are simply harder to evaluate because they publish fewer metrics. But that itself becomes a GTM issue. In a market where trust is scarce, silence creates friction.

For founders and marketers building consumer products, the lesson is broader than Web3.

You do not win by generating attention once. You win by making the product easier to believe, easier to try, easier to use, and easier to talk about.

That is the real GTM work.

Author note

Written by Stacy Muur, founder of Green Dots. I use Green Dots Research to document what we see across GTM strategy, creator-led distribution, founder growth, and Web3 marketing.