LATAM Stablecoin Adoption: How Web3 Teams Should Reach Users

Most Web3 teams treat LATAM stablecoin adoption as a remittance story. That is too narrow. The real opportunity is the daily dollar balance: where users hold it, how they spend it, and which products they trust after the money lands.

Most fintech decks about LATAM remittance start with the same slide: huge market, high fees, underbanked users, stablecoins as the new rail.

The slide is not wrong. It is just incomplete.

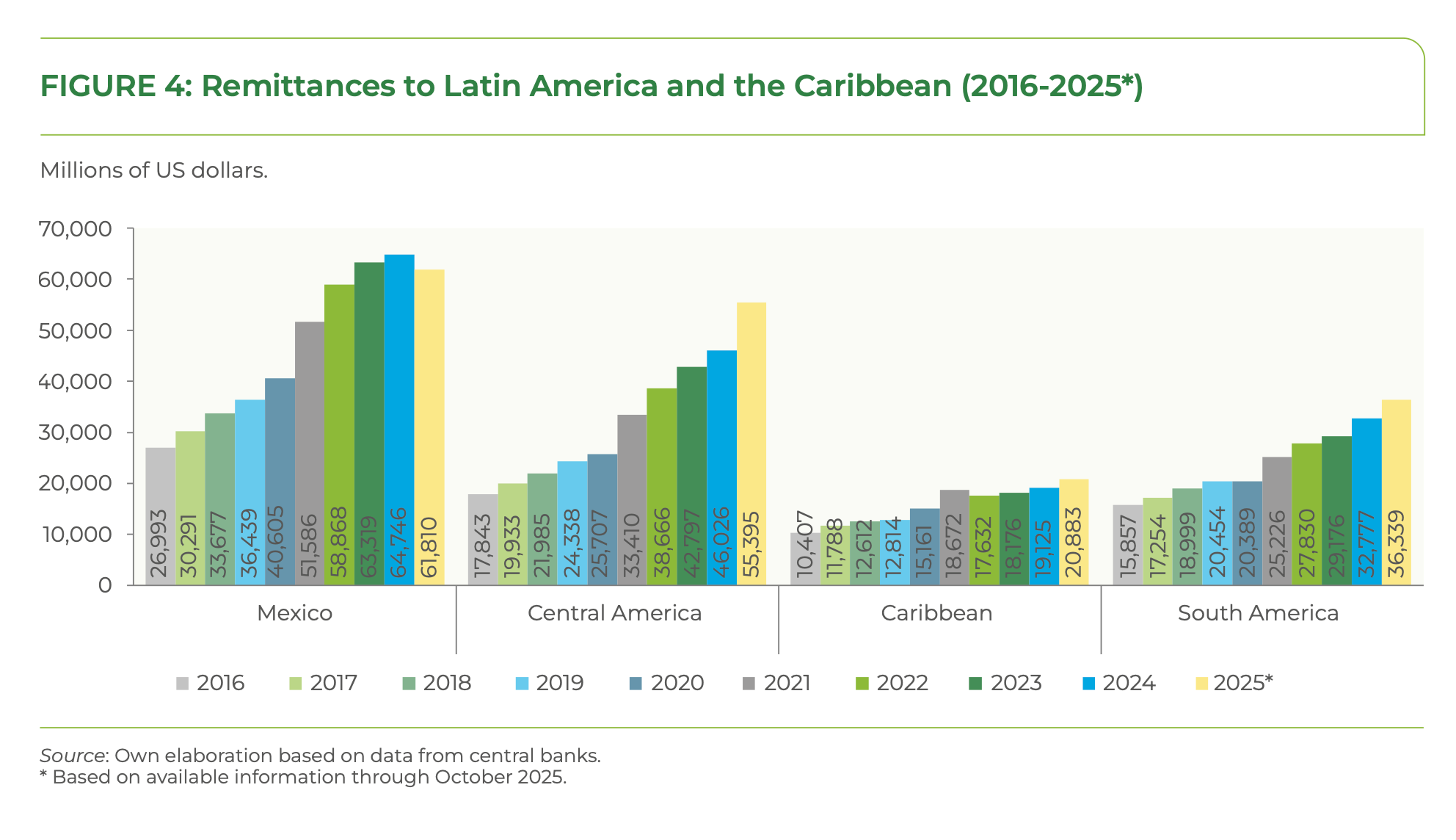

LATAM remittances are still growing. The Inter-American Development Bank expects remittances to Latin America and the Caribbean to reach $174.4 billion in 2025, up 7.2% from 2024, and equal to roughly 2.5% of regional GDP.

But the real opportunity is not “build a cheaper transfer app and win.” That is too narrow.

The better question is: who owns the dollar balance after the money lands?

Stablecoin adoption in LATAM is already past the awareness phase. Users are not waiting to be convinced that digital dollars are useful. In many markets, they already understand the problem: local currency volatility, limited dollar access, expensive cross-border movement, and weak financial infrastructure.

The remaining question is where they will hold, spend, and trust that balance.

Green Dots Research documents what we see across Web3 GTM strategy, creator-led distribution, founder growth, user acquisition, and market adoption.

Subscribe to get new field notes when they go live.

The remittance map is changing

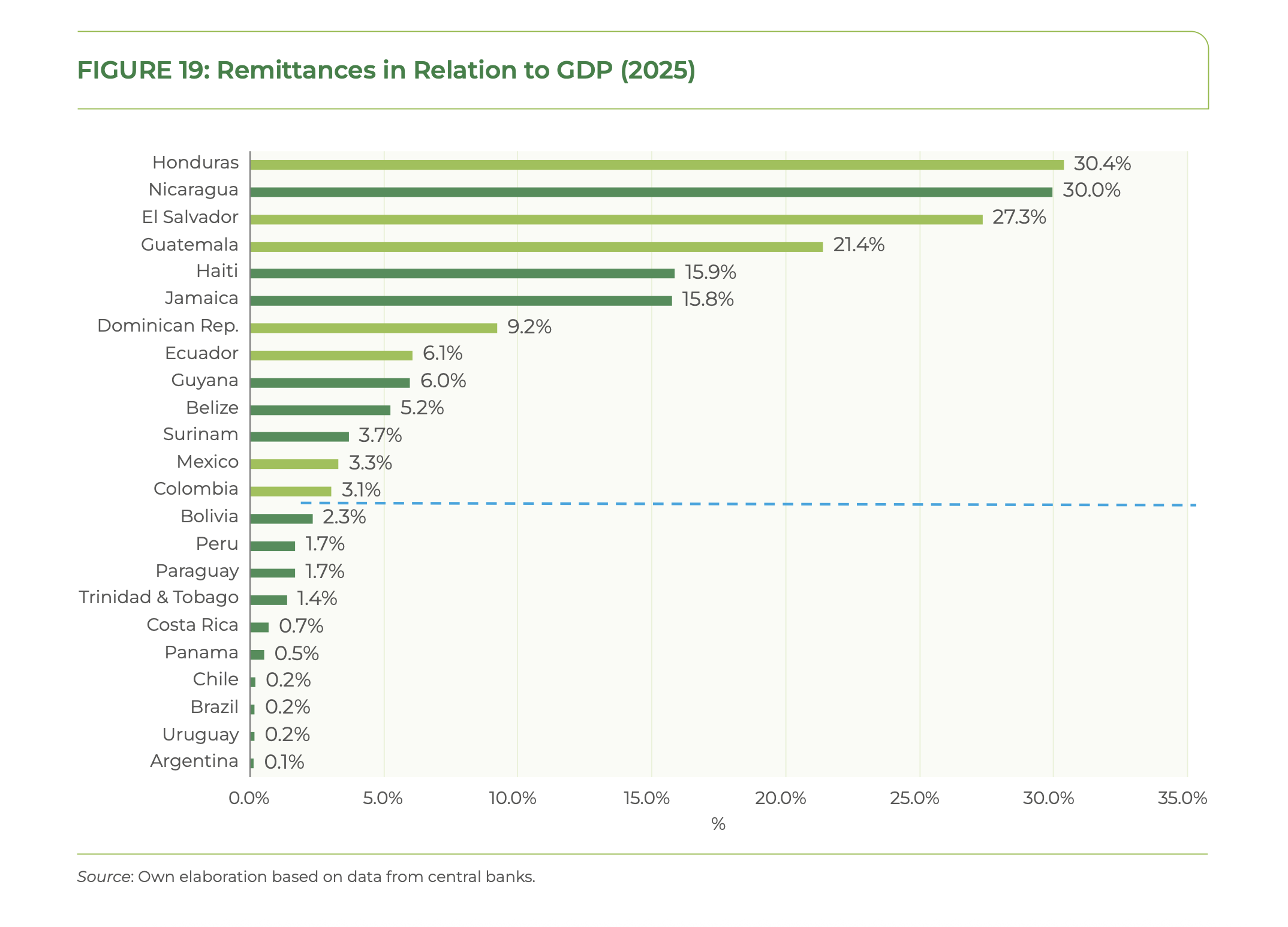

Mexico is still the largest remittance market in the region. But using Mexico as the default LATAM remittance proxy can lead teams into a shallow GTM strategy.

In 2025, IDB estimates remittances to Mexico will decline by around 4.5%, reaching about $61.8 billion. Mexico still represents 35.4% of regional remittances, but the direction matters. IDB points to a mix of base effects, exchange-rate dynamics, and changes in the Mexican migrant labor force as part of the explanation.

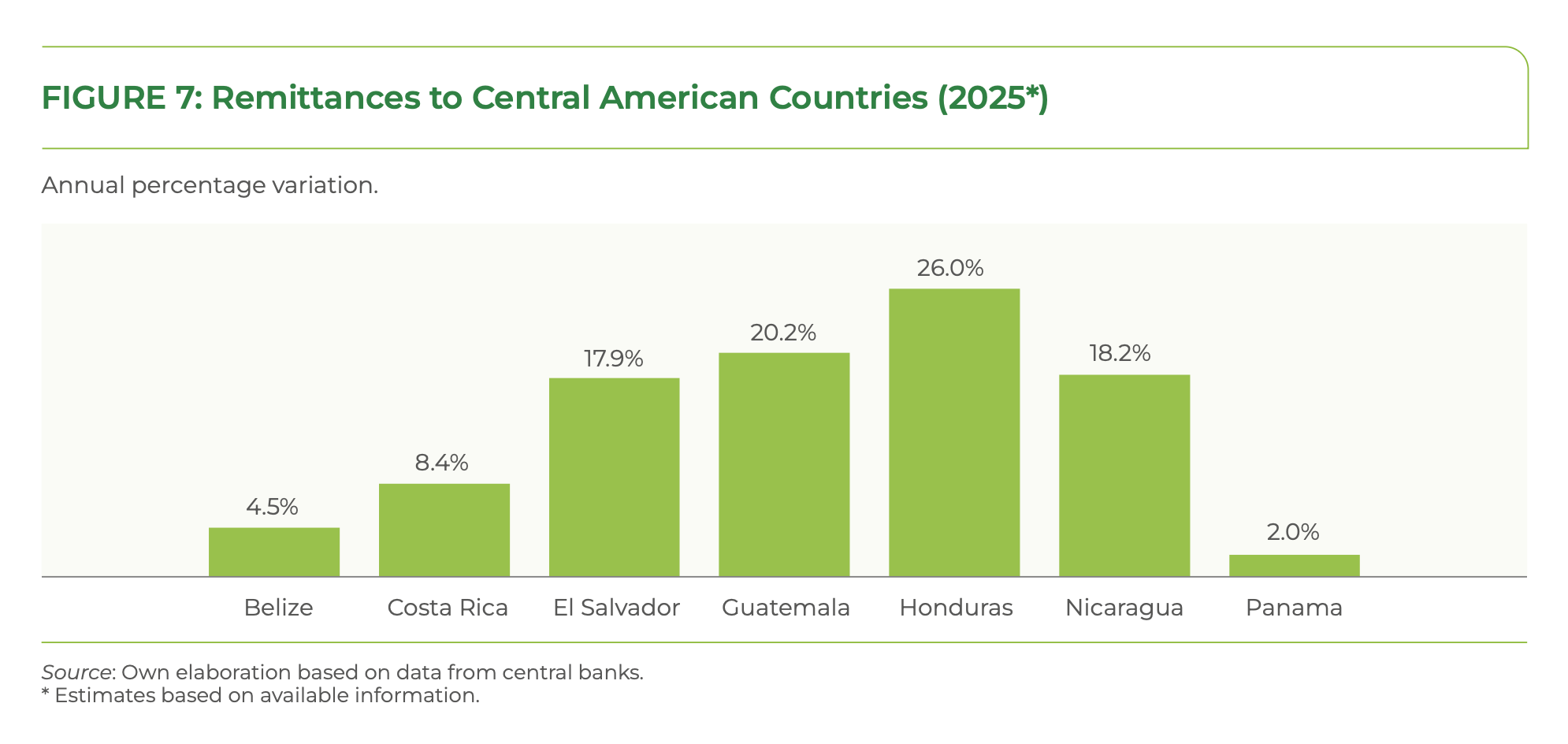

At the same time, Central America is moving differently. IDB reports that Central America recorded the strongest increases in 2025, with Honduras, Guatemala, Nicaragua, and El Salvador among the countries with the largest growth. The report estimates Central American remittance growth at 20.4% for 2025.

That changes the market map.

A fintech team that says “LATAM remittance” but only understands US → Mexico is not really building for LATAM. It is building for one dominant historical corridor.

The less served opportunity may sit in messier, more fragmented corridors: regional migration flows, Europe-to-LATAM flows, and country pairs that are not prioritized by the largest US-licensed money transfer operators.

This is where crypto rails and stablecoin liquidity become more interesting. Not because every user wants to “use crypto,” but because traditional financial infrastructure is uneven across corridors.

The user is not a crypto-native trader

A lot of stablecoin products are still designed as if the user is a 25-year-old crypto trader.

That is usually the wrong mental model for remittance.

The operational user is often older, trust-sensitive, and sending money for household needs. The recipient may be a parent, spouse, or family member who does not care about blockchain rails and does not want product complexity.

IDB household analysis shows that remittances often reach households led by older heads of household. The report also emphasizes that remittance flows remain an essential component of household income and consumption across the region.

That should shape product strategy.

If a 55-year-old sender has to think too hard before sending money home, the product has already failed.

The user does not want a wallet abstraction lecture. They want to know:

Can I send the money safely?

Will it arrive?

Can my family use it?

Will the value hold?

Can I trust this app with my salary or savings?

In remittance, trust is not a brand adjective. It is the product.

This is where many crypto and fintech teams overbuild the wrong features. They add on-chain options, token screens, advanced yield products, or “Web3” language before the core trust loop is solved.

For this market, simple beats impressive.

Stablecoins are becoming balance infrastructure

The biggest misunderstanding is treating stablecoins only as transaction rails.

Stablecoins are useful for settlement, cross-border transfer, treasury movement, and FX. But in LATAM, their deeper role is access to dollar-denominated balance.

Bitso’s 2025 Crypto Landscape report found that dollar-linked stablecoins became the most purchased crypto assets across its LATAM markets. USDC represented 24% of purchases, USDT 16%, and Bitcoin 18%. The report is based on behavioral data from nearly 10 million retail users across Argentina, Brazil, Colombia, and Mexico.

Bitso frames the shift as a move from speculation toward financial infrastructure for savings, payments, and cross-border value transfer. It also notes that users are using crypto in two ways at once: to access dollars and to accumulate long-term assets.

That distinction matters.

A user who buys stablecoins is not always trying to “make a crypto transaction.” Often, they are trying to hold dollars without relying on a fragile local path into dollars.

This changes the product category.

The transfer is only one moment. The balance is the relationship.

Why faster remittance is not enough

A faster remittance product can still lose if it does not own the next user action.

After the transfer lands, what happens?

Does the recipient cash out immediately?

Do they hold dollars?

Do they spend through a card?

Do they pay bills?

Do they convert slowly into local currency?

Do they earn on idle balance?

Do they send part of it onward?

Most remittance products monetize the movement of money. But stablecoin-native fintech products can compete for the balance layer.

That is more valuable because it creates repeated use.

If the user only opens the product once per month to send money, the product has a transaction relationship. If the user holds dollars there, spends from the account, receives money there, and checks the balance every week, the product has a financial relationship.

That is the real LATAM stablecoin opportunity.

Not “stablecoins make remittance cheaper.”

More specifically: stablecoins can turn remittance from a transfer event into an account relationship.

For crypto card products, LATAM can convert when the offer matches the real user behavior.

In a Green Dots campaign for Ether.fi Cash, a crypto card / neobank product, LATAM was the best-converting region and came in below the campaign’s average CAC.

The campaign activated around 15 creators and channels using a hybrid compensation model: fixed creator fees plus performance incentives. The rollout was sequenced in three stages:

Narrative seeding → amplification → conversion push

The goal was not only visibility. The campaign needed to explain why users should care about a crypto card, create enough trust around the product, and push toward registration.

Campaign results:

- Total budget: $25,000

- Registrations: 560 users

- Total user spend: $45,000 in two weeks

- CAC: ~$44.6 per user

- Spend per user: ~$80 in two weeks

The useful signal was not only the registration volume. It was that LATAM users converted and spent when the product connected to a real need: holding and spending dollar-linked value in a familiar way.

What this suggests: LATAM stablecoin adoption is not only a remittance story. The stronger opportunity may be products that turn dollar balances into daily financial accounts.

The product stack that can win in LATAM

The winning product will not be only a wallet, only a transfer app, or only a card.

It needs a stack.

1. Local rails, country by country

LATAM is not one market. Brazil, Mexico, Colombia, Argentina, Guatemala, Ecuador, and El Salvador are different operating environments.

A serious product needs local pay-in and pay-out rails. The user may not care whether the backend uses stablecoins, but they care deeply whether money can move through familiar local systems.

Without local rails, stablecoin UX collapses at the edge.

2. Stablecoin liquidity at scale

Stablecoins are only useful if users can enter and exit without bad spreads, delays, or confusing conversion paths.

Liquidity is a product feature.

Bitso Business’ 2025 stablecoin report argues that LATAM stablecoin adoption is moving from experimentation into operating infrastructure, with FX, treasury, and arbitrage accounting for 45% of processed volume among its institutional sample.

For remittance and consumer fintech, the lesson is simple: the backend matters. Users may never see liquidity, but they feel it through price, speed, and reliability.

3. A card or spend layer

If users hold digital dollars but cannot spend them, the product forces them back into cash-out behavior.

That weakens retention.

A card layer, bill-pay layer, or merchant spend layer turns the stablecoin balance into something usable in daily life. This is where stablecoin products move from “crypto wallet” to financial account.

4. Earn or yield, carefully designed

Yield can be useful, but it is also dangerous if framed badly.

For a risk-sensitive remittance user, yield should not feel like DeFi speculation. It should feel understandable, conservative, and optional. The wrong yield product can destroy trust faster than it improves retention.

In this category, trust is worth more than a few extra basis points.

5. Simple UX and trust cues

The product has to work for someone who is not crypto-native.

That means clear language, familiar flows, visible support, transparent fees, and no unnecessary complexity.

The best stablecoin product in LATAM may not look like a crypto product at all.

What fintech teams should ask before building

Before building another LATAM remittance or stablecoin product, teams should answer sharper questions.

Which corridor are we actually targeting?

Not “LATAM.” Which sender country, recipient country, currency pair, and migration flow?

Who is the recipient?

A trader, a parent, a household manager, a small merchant, a freelancer, or a family member receiving monthly support?

What is the user’s risk tolerance?

If the answer is close to zero, product language, onboarding, compliance, support, and custody all need to reflect that.

Do users want to move dollars or hold dollars?

This is the central product question. A transfer product and a balance product have different retention loops.

Do we have local rails?

Stablecoin liquidity is not enough if users cannot enter, exit, and spend through familiar systems.

Do we have enough liquidity to make the experience feel stable?

Bad pricing breaks trust.

Can a non-crypto user complete the action in under a minute?

If the answer is no, the product is probably too complex.

Stablecoin adoption already happened. The balance layer is still open.

The debate over whether LATAM users will hold digital dollars is becoming less interesting.

They already do.

The more important question is where that balance will live.

The products that win will not only move money faster. They will make the post-remittance balance useful: hold it, spend it, protect it, and move it again when needed.

That requires more than crypto rails. It requires corridor understanding, local infrastructure, liquidity, consumer trust, and a product that does not make the user feel like they are taking a risk every time they send money home.

The next phase of LATAM fintech will be won by the teams that understand this distinction:

The transfer gets attention. The balance wins the user.

Subscribe to get new field notes when they go live.

Author note

This piece is written by Stacy Muur, founder of Green Dots, based on the article from Claudia on X. Green Dots works with Web3 teams on GTM strategy, creator-led distribution, founder growth, and launch architecture.