Influencer Marketing Benchmarks for Fintech and Web3: CPM, CR, UAC, and KOL Pricing in 2025–2026

Influencer marketing benchmarks in fintech and Web3 should not stop at CPM. This article compares 2025–2026 CPM, CPA, UAC, conversion rates, and KOL pricing, showing how teams can measure creators by qualified action, not vanity reach.

Everyone wants a simple CPM benchmark for influencer marketing.

I get it. CPM is easy to compare. It gives marketers a quick way to judge whether a creator looks cheap or expensive against paid social, paid search, or another KOL campaign.

But in fintech, payments, finance, and Web3, CPM is only the cost of attention.

A cheap CPM can still bring weak users. A high-CPM creator can still be efficient if the audience trusts them enough to complete KYC, deposit funds, connect a wallet, sign a transaction, order a card, book a demo, join a community, or stay active after the campaign.

That is why influencer marketing benchmarks in these categories need a different standard.

This article has two parts:

- Benchmark overview: paid media baselines, creator pricing, CPM ranges, and what “good” can look like.

- Practical playbook: how to improve KOL campaign results instead of only reporting views.

Part 1: Benchmark overview

Why fintech and Web3 KOL benchmarks are difficult

With creators and KOLs, the brand is buying distribution through someone else’s trust, what changes the benchmark.

In fintech and Web3, the user journey is usually high-friction. A user does not simply click and buy. They may need to understand how the product works, trust the company, verify identity, connect a wallet, deposit funds, compare risks, read terms, or take a financial action.

That means a KOL campaign can be judged by many different events:

- impressions;

- views;

- clicks;

- app installs;

- signups;

- KYC completions;

- first deposits;

- wallet connects;

- first transactions;

- card orders;

- community joins;

- referrals;

- Day 7 or Day 30 retention;

- revenue per user.

This is why CPM alone is weak. A creator with expensive CPM can drive expensive views and better activation.

Paid media benchmarks to compare KOL campaigns against

Before judging whether a KOL is expensive, marketers need a baseline.

Paid media is not a perfect comparison, but it gives teams a reality check. If paid search can produce qualified leads at a certain cost, a creator campaign needs to explain why its cost is better, worse, or justified by higher trust and user quality.

| Channel / source | Benchmark | Practical read |

|---|---|---|

| Google Search, all industries – WordStream 2025 | CTR: 6.66%; CPC: $5.26; conversion rate: 7.52%; CPL: $70.11 | Useful baseline for intent-driven acquisition. |

| Finance & Insurance Google Search – WordStream 2025 | CPL: $83.93 | Fintech KOL campaigns near or below this qualified cost can be competitive. |

| Facebook lead campaigns – WordStream 2025 | CTR: 2.59%; CPC: $1.92; conversion rate: 7.72%; CPL: $27.66 | Cheap leads are not the same as verified or activated users. |

| Facebook traffic campaigns – WordStream 2025 | CPC: $0.70; CTR: 1.71% | Good for traffic comparison, weak for true fintech acquisition. |

| Gupta Media paid social tracker | TikTok CPM: $4.67 in Oct 2025; Meta CPM: $8.37 in Sep 2025 | Paid social CPMs can look much cheaper than creator pricing. |

| Prooflytics 2026 directional CPMs | Meta: $6–$15; TikTok: $10–$20; LinkedIn: $30–$60; YouTube in-stream: $5–$15 | LinkedIn and finance audiences need to be judged against lead quality, not CPM alone. |

| Lever Digital fintech benchmarks | Fintech conversion rate: 5–10%; CPA: $50–$150 | Useful range for fintech acquisition planning. |

| Marketer.co / MarketersMedia fintech report | CPA: $50–$150 for high-performing campaigns; landing page conversion: 8–18%; awareness CPM: around $11.50 | Supports the same practical CPA range. |

The practical read is simple:

- Qualified UAC below $50 is unusually efficient for fintech or Web3.

- $50–$150 qualified UAC may be normal or acceptable, depending on geo, funnel, product margin, and user quality.

- Above $150 needs LTV justification.

- Install cost should not be confused with acquisition cost.

- A “lead” is not the same as a funded account, verified user, active wallet, or retained customer.

That last point matters.

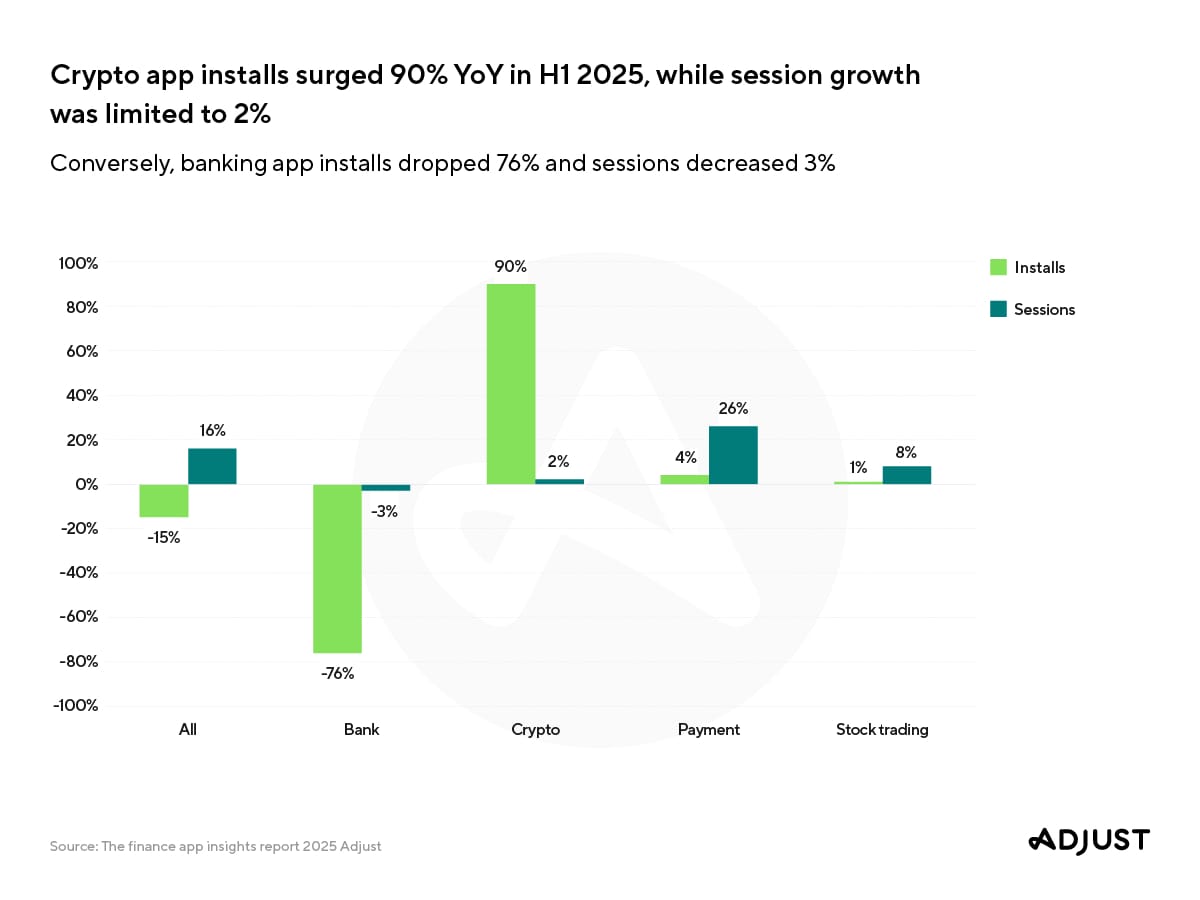

Adjust reported that finance app installs grew 11% year over year globally in Q3 2025, payment apps accounted for 58% of finance app sessions from 2024 through H1 2025, and crypto app installs grew 90% year over year in H1 2025.

AppTweak’s 2025 Finance App Insights Snapshot reported a 6.1% tap-through rate for U.S. finance apps, a 4.5% global TTR average, France CPT at $2.11, and CPT above $6.00 in the U.K. and South Korea.

So if the campaign stops measuring at install, the benchmark is too shallow.

What KOL pricing looks like across platforms

Creator pricing depends on platform, niche, audience quality, format, engagement, exclusivity, usage rights, geography, and whether the deal includes a performance component.

Use this formula:

KOL implied CPM = campaign fee ÷ actual views × 1,000

Example:

If a creator charges $5,000 and the post receives 100,000 views, the implied CPM is $50.

That implied CPM should be compared against paid social CPM, category CPM, click-through rate, qualified conversion rate, UAC, retention, and revenue quality.

Here is the benchmark view by platform:

| Platform / creator type | Reported pricing or CPM | Best use case |

|---|---|---|

| Instagram / Reels | Collabstr reported Instagram collaborations around $364 in 2025, with Reels around $288. InfluenceFlow places Instagram CPM around $5–$15. | Trust-building, lifestyle finance positioning, demos, social proof, retargeting creative. |

| TikTok | Collabstr reported TikTok collaborations around $350 and TikTok videos around $217. InfluenceFlow places TikTok CPM around $2–$8. | Awareness, younger retail users, app installs, waitlists, simple offers, short educational hooks. |

| YouTube finance creators | InfluenceFlow estimates finance YouTube CPM around $40–$100, with long-form integrations often ranging from $2,000 to $50,000+. | High-consideration finance products, wallets, cards, investing tools, security explainers, education-led conversion. |

| LinkedIn B2B finance / fintech creators | InfluenceFlow reports B2B creators charging $2,000–$25,000 per sponsored post, with 30–50% premiums over equivalent B2C creators. | B2B payments, embedded finance, compliance tech, banking infra, partnerships, investor-facing credibility. |

| X / Twitter Web3 KOLs | AP Collective estimates X pricing from $500 to $50,000+ per post. | Narrative shaping, launch announcements, ecosystem attention, community momentum, token or product catalysts. |

| Telegram Web3 communities | AP Collective estimates Telegram pricing around $500–$5,000 per post. | Direct community activation, alpha groups, announcements, referral campaigns, wallet actions, short-term conversion spikes. |

| Web3 micro / mid / top-tier KOLs | MEXC estimates micro KOLs at $500–$2,000 per post, mid-tier creators at $3,000–$8,000, and large campaigns with top-tier influencers or AMAs at $20,000–$50,000+. | Micro: niche trust and acquisition. Mid-tier: narrative and validation. Top-tier: launch awareness and market signal. |

One important nuance: a $60 CPM finance YouTube creator may look expensive next to a $5 TikTok CPM. But if the YouTube audience converts to KYC, deposit, subscription, or retained usage at a much higher rate, the effective UAC can be better.

This is where many fintech and Web3 teams misread the campaign: they judge the creator by the cost of attention before checking whether the audience took the action that matters.

Why CPM alone is not enough

Use this simple example.

| Metric | Creator A | Creator B |

|---|---|---|

| Fee | $2,000 | $5,000 |

| Views | 400,000 | 100,000 |

| Implied CPM | $5 | $50 |

| Qualified users | 10 | 100 |

| Qualified UAC | $200 | $50 |

Creator A looks cheap on CPM, while Creator B looks expensive on CPM. But Creator B produces a much better acquisition cost.

Metrics every KOL campaign should track

A useful KOL dashboard should separate attention, intent, activation, and quality.

| Metric | Formula | What it tells you |

|---|---|---|

| Implied CPM | Campaign fee ÷ actual views × 1,000 | Cost of actual creator reach. |

| CTR | Clicks ÷ views | Whether the hook, format, and CTA made people act. |

| Landing page conversion rate | Signups ÷ clicks | Whether the page and offer matched the audience. |

| Qualified conversion rate | Qualified users ÷ clicks | Whether traffic became real users. |

| Qualified UAC / effective CPA | Total campaign cost ÷ qualified users | Main efficiency metric for acquisition-focused campaigns. |

| Activation rate | Activated users ÷ signups | Whether signups reached the real business event. |

| Retention / quality | Day 7 retention, Day 30 retention, deposit rate, transaction rate, wallet activity, revenue per user, referral behavior | Whether the creator produced real users or vanity conversions. |

Activation should be defined before the campaign starts.

For fintech, activation may mean KYC completion, first deposit, card order, first transaction, subscription start, or demo booked.

For Web3, activation may mean wallet connect, deposit, swap, staking action, borrowing action, governance participation, referral, or repeat usage after incentives decline.

Want to get more research like this directly into your inbox?

Don't hesitate to subscribe. It's absolutely free.

Part 2: How to improve KOL campaign results

1. Treat every creator activation as a micro-campaign

In our work with Web3 teams, the campaign usually breaks because the creator, audience, offer, landing page, tracking, and activation goal were not designed as one system.

Do not give every creator the same script, landing page, and CTA.

The better operating model is: creator-specific hook → creator-specific landing page → creator-specific CTA → creator-specific tracking → creator-specific benchmark.

Here is how that changes by channel.

| Creator type | Better campaign angle | Best-fit goal |

|---|---|---|

| Finance educator on YouTube | Detailed explainer: how the product works, who it is for, what users should understand before signing up. | Trust, qualified conversion, deposit, subscription, demo request. |

| TikTok money creator | Simple problem-led hook with one pain point and one benefit. | Reach, app installs, waitlist signups, low-friction trial. |

| Web3 X account | Narrative and catalyst angle: why this matters now, how it fits the market, what the audience can do next. | Wallet connects, community joins, launch momentum, ecosystem attention. |

| LinkedIn fintech operator | Business-case angle: compliance impact, cost savings, infrastructure value, partner relevance. | Demo requests, partnership leads, investor credibility, B2B pipeline. |

| Telegram alpha group | Direct activation angle: clear, time-bound, easy to act on. | Claims, referrals, wallet actions, signups, community activation. |

Margin note: buying one post is the weak version. Building one creator-specific funnel is the stronger version.

2. Segment KOLs by campaign goal

Do not judge every KOL by the same CPA. Some creators are good at reach. Some are good at narrative. Some are good at trust. Some are good at conversion.

Segment creators before the campaign starts.

| Awareness KOLs | |

| Main job | Create reach and recognition. |

| Common formats | TikTok, Instagram Reels, large X accounts, short-form video, meme pages. |

| Primary KPIs | CPM, reach, views, view-through rate, branded search lift, follower growth, retargeting pool growth. |

| Cost logic | Lower CPM matters more. Direct UAC may be weak, but the creator can still feed retargeting. |

| Narrative KOLs | |

| Main job | Explain why the product matters now. |

| Common formats | X threads, YouTube explainers, LinkedIn posts, podcasts, newsletters, founder interviews. |

| Primary KPIs | Engagement quality, saves, comments, watch time, community joins, sentiment, quality of discussion. |

| Cost logic | Higher CPM can be acceptable if understanding and trust improve. |

| Acquisition KOLs | |

| Main job | Drive measurable users. |

| Common formats | Micro creators, niche affiliates, Telegram groups, direct-response TikTok, YouTube mid-roll offers, newsletter sponsorships. |

| Primary KPIs | Qualified UAC, signup rate, KYC completion, wallet connect, first transaction, first deposit, trial start. |

| Cost logic | Judge closest to paid acquisition benchmarks. These creators need to compete with or beat the $50–$150 qualified CPA range. |

| Trust KOLs | |

| Main job | Reduce perceived risk. |

| Common formats | Finance educators, analysts, operators, security voices, compliance voices, long-form YouTube, podcasts, LinkedIn experts. |

| Primary KPIs | Qualified conversion rate, deposit rate, demo quality, retention, sales conversations, LTV, objection reduction. |

| Cost logic | Highest CPM may be justified if user quality is stronger. |

This avoids one of the most common KOL mistakes: forcing every creator into a direct-response benchmark.

3. Let creators shape the format

The creator should not only distribute the message. They should help shape it.

Tinuiti’s Q3 2025 Digital Ads Benchmark Report found that Facebook Reels video ads doubled their impression share year over year, from 7% in Q3 2024 to 14% in Q3 2025.

Before launch, ask the creator:

- What format would your audience actually trust?

- What objections will they have?

- What CTA would feel native?

- What offer would make them click now?

- What should we avoid saying?

- Should this be a short post, thread, long-form explainer, live session, AMA, tutorial, story sequence, or pinned community post?

- Would the audience prefer education, comparison, founder story, product walkthrough, or exclusive perk?

The best-performing activation is the one that feels native to the creator’s community.

4. Give each KOL audience a specific perk

A generic CTA like “sign up with this link” is weak.

A creator-specific offer gives the audience a reason to act and gives the brand cleaner attribution.

Examples:

| Product type | Better creator-specific perks |

|---|---|

| Fintech app | Fee-free period, premium trial, cashback boost, early access, invite-only onboarding, founder Q&A, free consultation. |

| Payments product | Discounted card, free first transaction, merchant reward, referral bonus, higher cashback, limited-time fee waiver. |

| Web3 wallet or app | Gas rebate, points boost, allowlist access, fee discount, early feature access, NFT or badge, priority access, community role. |

| B2B fintech | Free audit, extended pilot, founder/operator office hours, private benchmark report, integration consultation, discounted first month. |

| Investing or trading product | Educational pack, premium analytics trial, risk disclosure webinar, lower platform fee, strategy session, private product walkthrough. |

The offer should match the campaign goal.

- If the goal is trust, use education, founder access, or a product walkthrough.

- If the goal is activation, use a perk tied to KYC, first deposit, first transaction, wallet action, or trial start.

- If the goal is community quality, avoid generic rewards that attract people who only want the prize.

5. Start with pilots, then renew based on quality

The first activation should be treated as a pilot benchmark, not the final answer.

Influencer Marketing Hub’s 2025 report says experts emphasize a 47% focus on long-term influencer partnerships. InfluenceFlow also describes the rise of hybrid deal structures with base payments, performance bonuses, commission, and exclusivity fees.

A one-off post can be useful for testing. Efficiency usually improves through iteration.

A simple structure:

Pilot activation

- Flat fee.

- Goal: establish baseline.

- Track views, clicks, signups, KYC, wallet connects, deposits, transactions, community joins, or demo requests.

Second activation

- Flat fee plus performance bonus.

- Goal: improve against the pilot.

- Bonus if qualified users increase meaningfully.

Long-term deal

- Lower base fee plus performance bonus.

- Goal: reward repeat performance and user quality.

- Bonus tiers can be tied to KYC completion, first deposit, transaction, retention, revenue, or community quality.

Ambassador phase

- Monthly retainer plus CPA or revenue-share component.

- Use only for creators who have already proven acquisition quality.

Example: if the pilot generated 10 qualified users, the renewal can include a bonus at 20 qualified users, a higher bonus at 30 qualified users, and a quality bonus if those users complete KYC, deposit, transact, or remain active after 30 days.

Benchmark KOLs against themselves. A creator who improves from 10 to 20 qualified users after better messaging may be more valuable than a creator who produced one lucky spike and then declined.

6. Diagnose campaign results by failure pattern

After every activation, place the KOL into one of these categories.

| Result pattern | What it means | What to test next |

|---|---|---|

| Low CPM, low conversion | Cheap attention, weak acquisition. | Keep as awareness only, or test stronger hook, better CTA, better offer, retargeting, or new format. |

| High CPM, high qualified conversion | Expensive reach, strong user quality. | Consider renewal, bonus structure, deeper explainer, better landing page, retention-based incentive. |

| High CTR, low conversion | Creator created interest, but the funnel leaked. | Fix landing page alignment, offer clarity, onboarding, trust signals, signup speed, audience fit. |

| Low CTR, high conversion | Audience quality may be strong, but the hook is weak. | Test better opening line, stronger visual, more native format, creator-led script, sharper perk. |

| High signups, low activation | The campaign produced curiosity, not qualified users. | Improve education, qualification, onboarding, realistic messaging, and incentives tied to activation instead of signup. |

| Strong first activation | The creator has potential. | Move to second campaign with better creative, creator-specific landing page, retargeting, deeper demo, and performance bonus. |

This is where campaign learning becomes useful.

You should ask where the system broke: creator, audience, message, offer, landing page, onboarding, attribution, or product fit.

Directional benchmark ranges for fintech and Web3 KOL campaigns

| Benchmark | Directional range / read |

|---|---|

| Paid social CPM | Often around $5–$15 on major consumer platforms, though methodology varies by source and platform. |

| LinkedIn / B2B finance CPM | Usually much higher; judge against qualified lead value, not CPM alone. |

| Fintech paid acquisition CPA | Often around $50–$150 depending on geo, product, funnel, and event definition. |

| Finance & Insurance search CPL | Can exceed $80, which makes strong KOL campaigns competitive if they produce qualified users near or below that range. |

| YouTube finance creators | Often much higher CPM, around $40–$100, because long-form supports trust and education. |

| Web3 KOL pricing | Can range from hundreds of dollars for micro placements to tens of thousands for top-tier creators, AMAs, or launch activations. |

| App installs | Can be much lower than true fintech acquisition cost; measure activation, not just installs. |

These ranges should not be treated as universal targets. They are planning references.

Always adjust benchmarks by:

- geography;

- platform;

- product type;

- funnel complexity;

- audience trust;

- creator niche;

- attribution quality;

- offer strength;

- compliance constraints;

- activation event;

- user LTV.

Final takeaway: benchmark for qualified action, not vanity reach

The strongest fintech and Web3 teams will treat each creator as a micro-campaign.

The operating model is simple:

- start with a pilot;

- track actual views, clicks, signups, and qualified users;

- calculate implied CPM and qualified UAC;

- segment creators by role;

- customize the message and offer;

- renew only the creators who improve against their own benchmark;

- add bonuses for qualified user growth, not vanity engagement.

In fintech, payments, finance, and Web3, the best KOL is the creator who can repeatedly turn trust into qualified action.

Subscribe to get new field notes when they go live.

Author note

Written by Stacy Muur, founder of Green Dots. Green Dots works with Web3 teams on GTM strategy, creator-led distribution, founder growth, and launch architecture.