What Most Teams Misunderstand About Fintech User Acquisition

Fintech user acquisition usually breaks before the channel does: in trust, onboarding, activation, or timing. This article explains what teams should fix before scaling paid growth.

Most fintech user acquisition problems are diagnosed too late.

Teams usually notice the problem after CAC rises, paid channels stop scaling, referrals flatten, or KYC completion rates disappoint. By then, the channel gets blamed. Paid social is too expensive. Influencers did not convert. SEO is slow. Partnerships take too long.

Sometimes that diagnosis is correct.

More often, the channel is exposing a deeper problem: the product has not made trust, first use, and repeated use easy enough.

We’ve analysed research and case studies beyond our work at Green Dots to aggregate facts that support my long-standing internal thinking: fintech user acquisition isn’t decided by channel choice alone. It’s decided by the interaction of trust, onboarding friction, activation economics, and distribution advantage.

A fintech company can buy installs. It can’t buy durable users if the path from attention to first value is weak.

What is fintech user acquisition?

Fintech user acquisition is the process of attracting, converting, activating, and retaining users for financial products such as wallets, neobanks, payment apps, lending platforms, investing products, crypto exchanges, and embedded finance tools.

It differs from ordinary consumer app acquisition because financial products carry higher perceived risk.

Users often need to share sensitive data, pass identity checks, connect bank accounts, deposit funds, move salary, make a first payment, borrow money, or trust a platform with assets. That means acquisition does not end at signup. In many fintech products, the real acquisition event is first deposit, first trade, first funded loan, payroll switch, card provisioning, or first merchant transaction.

This is where many fintech growth models break.

A paid install is not a user.

A completed signup is not necessarily an activated customer.

A first transaction is not retention.

Why fintech user acquisition behaves differently

Our research points to four reasons fintech growth behaves differently from lower-stakes consumer software.

First, trust is a conversion variable. In wallets, banking, investing, lending, and crypto, users need to believe the provider before they act. The research shows that trust strongly shapes provider choice, especially in digital wallets, where large banks still hold a trust advantage over fintechs and large tech firms. In crypto, trust barriers are even more explicit: volatility, counterparty risk, platform viability, and support concerns all suppress adoption.

Second, regulation adds friction before monetization. KYC, AML checks, identity verification, affordability reviews, document uploads, sponsor-bank constraints, and compliance flows sit between acquisition and revenue. These are not edge cases. They are part of the funnel.

Third, consumer inertia is high. People do not wake up every week wanting to change banks, refinance debt, move brokerage accounts, or try a new wallet. Fintech switching is often event-driven: moving country, starting a job, graduating, shopping for a large purchase, refinancing, entering a market cycle, or needing a specific payment use case.

Fourth, activation often requires a second action. Many fintech products do not deliver value at account creation. They deliver value after funding, transfer, card use, repayment, investing, payment acceptance, or recurring behavior.

The practical implication is simple: fintech growth teams should not optimize only for acquisition cost. They should optimize for the cost of a trusted, activated, repeat user.

The funnel usually breaks before paid acquisition can work

Bain & Company documented a digital wallet case where more than 18 required data fields across five screens caused nearly half of would-be customers to abandon signup. After redesigning the experience into a simpler single-screen flow, the wallet increased first-deposit rate by 50% and generated a reported 20x return on fees.

That example matters because it shows the hidden cost of buying volume before fixing onboarding.

If a team pays for traffic into a high-friction funnel, the media channel looks inefficient. But the real problem may be the form, trust cues, KYC flow, unclear next step, or weak first-use prompt.

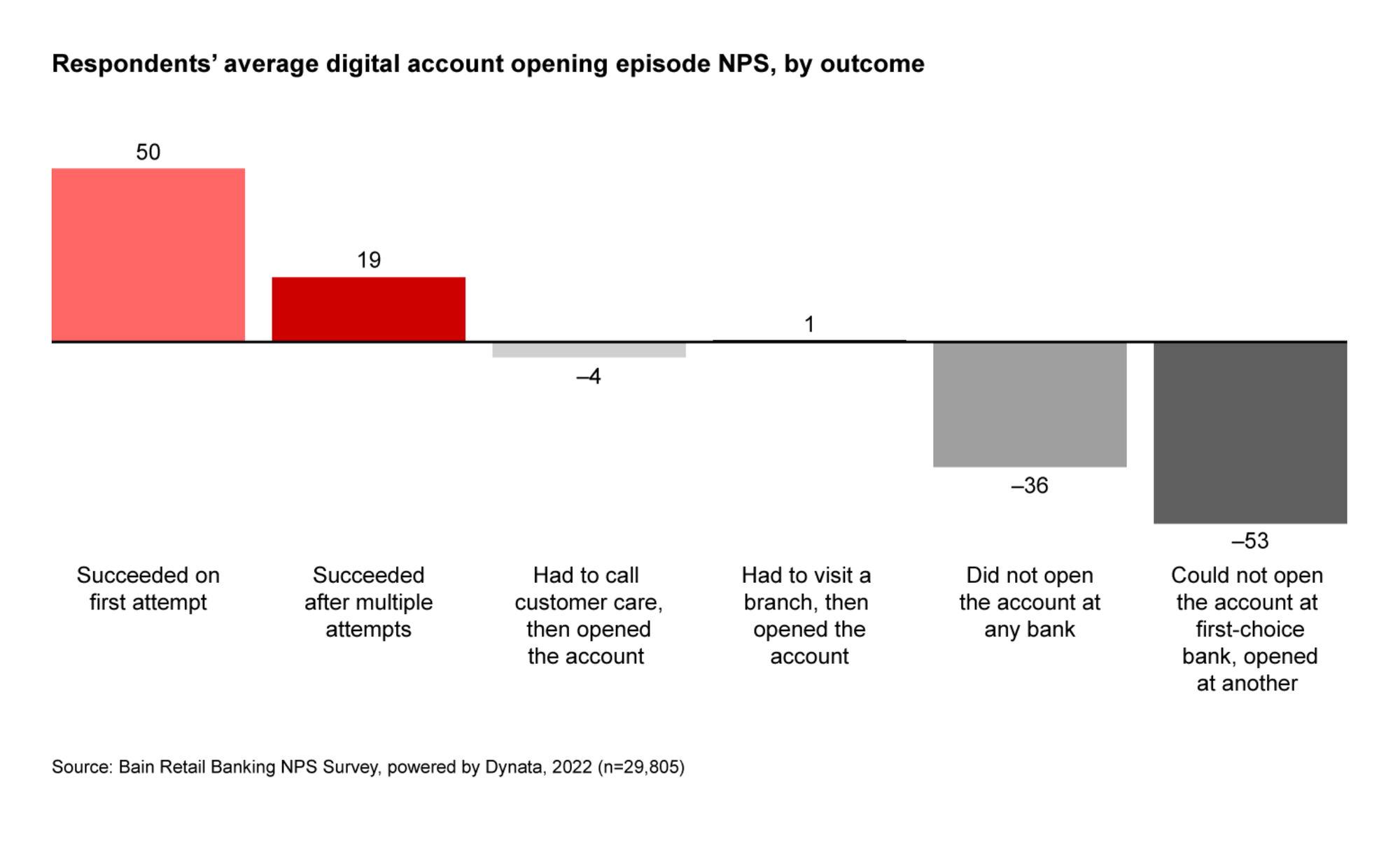

The same pattern appears in broader banking onboarding. Bain’s global banking loyalty research says that even in the strongest markets for account opening, the UK and Hong Kong, only about two-thirds of respondents successfully opened an account digitally on the first attempt.

For fintech teams, this should change the order of operations.

Before scaling paid acquisition, teams should know:

- How many installers become signups.

- How many signups pass KYC.

- How many verified users fund the account.

- How many funded users complete the first meaningful action.

- How many users repeat the action within the first week or month.

- Where trust, confusion, or effort causes drop-off.

This is not only a product analytics exercise. It is a GTM issue.

If the user does not understand why the product is safe, useful, and worth acting on now, acquisition spend will amplify the weakness.

We saw this clearly while designing the GTM strategy for a trading terminal in 2026.

KOLs were the main user acquisition layer for the product, so we treated Customer Development as stage zero. Before onboarding creators, we needed to validate what would make them switch from the tools they already trusted.

That process surfaced hidden pains that were not visible in the initial positioning. The protocol team had a clear product narrative, but the market cared about slightly different things: workflow cost, trust, credibility with their own audience, and whether switching would create more risk than upside.

This changed the positioning before the campaign started.

That is the point: in crypto, user acquisition often depends on understanding switching behavior before asking anyone to amplify the product.

Paid acquisition works best when intent already exists

Generic paid acquisition is overrated in fintech.

That does not mean paid channels are useless. It means paid works best when the product meets existing intent.

For neobanks, paid acquisition performs better around inflection points: starting work, relocating, becoming a student, opening a salary account, seeking better savings rates, or refinancing debt. For lending and investing platforms, paid works better when intent is already explicit: debt consolidation, brokerage comparison, student-loan refinance, or financing at checkout.

For crypto, paid channels are more sensitive to market conditions. They tend to work better in bull or recovery phases, when users already have elevated intent to trade, bridge, buy, or explore onchain products. But even there, paid traffic can become expensive before KYC, deposit, and first-trade leakage are counted.

AppTweak’s 2025 Apple Ads benchmarks show how expensive finance-app acquisition can become inside App Store search. Across countries and categories, the median Apple Ads search-results CPI was $1.80, while U.S. finance apps had a median CPI of $8.23 and a median CPT of $3.55. That cost is still only the install stage, before signup, KYC, funding, and first-use drop-off.

| APP CATEGORY | MEDIAN COST PER INSTALL (CPI) |

| Business | $5.80 |

| Education | $3.24 |

| Finance | $8.23 |

| Games | $12.28 |

| Graphics & Design | $3.68 |

| Health & Fitness | $3.83 |

| Lifestyle | $3.45 |

| Music | $2.11 |

| Photo & Video | $3.13 |

| Productivity | $3.13 |

| Social Networking | $3.90 |

| Sports | $26.81 |

| Shopping | $6.20 |

| Utilities | $2.90 |

The mistake is treating paid as demand creation when the product requires trust and timing.

Paid is strongest when it captures demand that is already present. It is weakest when it tries to convince a cold user to trust a complex financial product without enough context.

Embedded distribution often beats direct acquisition

One of the clearest patterns we have discovered is the strength of partnership-led and product-embedded distribution.

Embedded finance works because it places the financial product inside the user’s existing workflow. The user is already shopping, selling, paying, borrowing, managing payroll, accepting payments, or running a business process. The product appears at the point of need instead of asking the user to leave one context and enter another.

McKinsey research estimates that embedded-finance volumes in Europe have grown three times as fast as directly distributed loans over the past decade and could account for 20–25% of retail banking sales and retail/SME lending by 2030.

BNPL (buy now, pay later) shows the same pattern. McKinsey argues that leading Pay-in-4 providers are not simply financing checkout; they are building integrated shopping platforms that engage consumers from prepurchase to post-purchase.

In a separate consumer payments study, McKinsey found that 80% of BNPL users had started a shopping journey on a BNPL provider’s site rather than a retailer’s site, and 43% of BNPL transactions began with the provider. This makes BNPL an acquisition layer, not only a payment method.

For fintech teams, the lesson is not “do partnerships.” The lesson is sharper: distribution improves when the product sits near the moment where the financial need appears.

That may mean merchant checkout, payroll, vertical SaaS, marketplaces, telecoms, creator platforms, crypto wallets, exchanges, e-commerce flows, banking interfaces, or accounting tools.

The best acquisition channel may not look like a media channel at all.

Wallets win through frequency and acceptance

Payments and wallets behave differently from lending or investing because they can become habitual.

Wallet acquisition works best when the product is tied to a frequent, practical use case.

McKinsey’s 2024 Digital Payments Survey found that 74% of U.S. consumers and 71% of European consumers cited easier and faster checkout as a primary reason for using digital wallets, while roughly one-quarter of U.S. respondents said points and discounts influence payment choice. In Southeast Asia, McKinsey’s interviews with leaders from GCash, MoMo, and GrabPay show how adoption compounds after the first trust barrier is crossed: education and awareness make the product legible, then visible use by friends, family, and merchants turns wallets into a normal payment behavior.

This is why wallet growth depends so heavily on ecosystem conditions.

A wallet with strong merchant acceptance, cash-in/cash-out infrastructure, rewards, social sending, and repeated payment contexts has many routes to habit. A wallet without acceptance has to spend heavily to manufacture behavior that the product environment does not support.

For wallet teams, the acquisition question is not only “how do we get users?” It is “where does the wallet become the easiest next action?”

That may be P2P transfers, merchant payments, salary, remittances, rewards, social commerce, gaming, crypto rails, or super-app workflows.

Neobanks need primary relationship, not only account creation

Neobank acquisition often looks healthy at the top of the funnel and weak deeper down.

A user may open an account for a bonus, rate, travel feature, budgeting tool, or temporary use case. But the economics change when the neobank becomes the primary financial relationship.

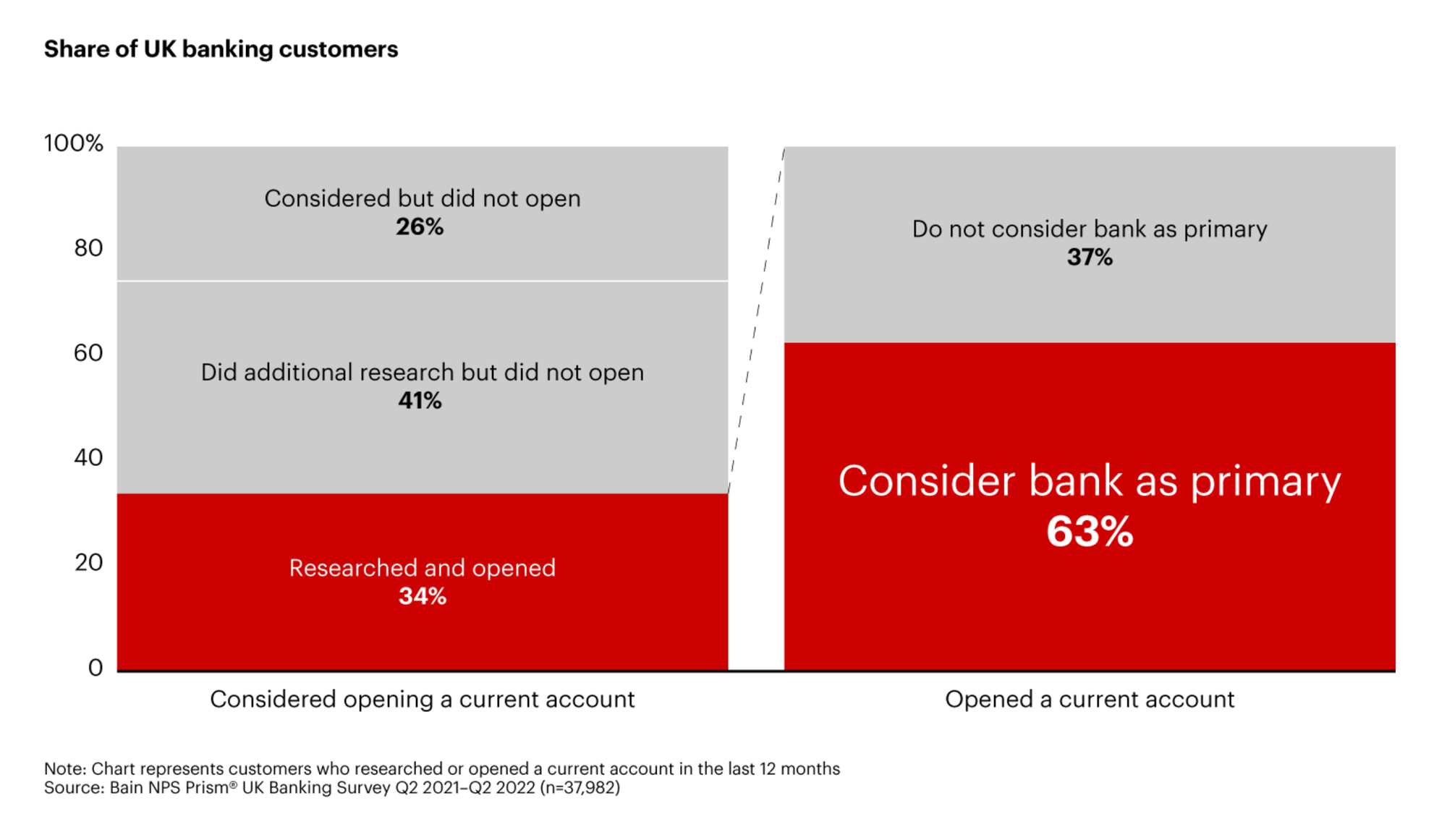

Bain’s UK banking analysis found that primary banking customers are more than three times as likely to hold multiple products with the bank and give the bank an average Net Promoter Score more than triple that of non-primary customers.

This is why neobank acquisition should be measured against primary-relationship behavior, not only signups:

- Payroll deposit.

- Recurring card usage.

- Bill payment.

- Savings balance.

- Multi-product adoption.

- Monthly active financial behavior.

- Referral after repeated use.

A neobank that buys signups without a path to primary usage is often buying low-intent secondary accounts.

Promotional rates can work, but the research also flags the risk of attracting rate optimizers. In that case, high-yield savings becomes CAC in another form.

Crypto user acquisition needs credibility, not only attention

Crypto is the fintech segment where attention is easiest to generate and trust is easiest to lose.

Paid campaigns, KOLs, referral programs, quests, airdrops, and community campaigns can all create visible activity. But visible activity can hide weak user quality.

Crypto user acquisition has to solve a sharper trust problem than most fintech categories.

McKinsey’s consumer payments research found that among respondents with no interest in owning crypto, 39% cited volatility as a barrier, while trust in the technology, trust in counterparties, long-term viability, and lack of support channels also appeared as adoption concerns.

A separate study on cryptocurrency trust dynamics uses the FTX collapse as a natural experiment and shows that major trust shocks can affect token valuation, trading flows, and sentiment across CEX and DEX environments. For crypto products, acquisition cannot be treated as attention buying alone. The user needs enough confidence to believe the platform, understand the risk, and take the first funded action.

This is where creator and KOL marketing need a more disciplined role.

For crypto products, the strongest acquisition systems usually combine:

- product education,

- credible creators,

- founder signal,

- clear risk framing,

- community support,

- referral mechanics,

- and a direct activation path.

A campaign that only buys reach may create noise. A campaign that builds understanding can create users.

Lending and investing need intent, education, and social risk awareness

Lending and investing products are high-consideration categories.

Users compare options. They worry about downside. They may need documents, eligibility checks, funding, repayment plans, portfolio setup, or risk understanding.

Broad top-of-funnel prospecting often performs poorly in fintech because many users are not actively looking to switch banks, refinance debt, open a brokerage account, or try a new financial product. a16z describes this as an “inflection point” problem: fintech acquisition works better when it reaches users at moments of heightened need, such as graduation, student-debt refinancing, relocation, or a major financial decision.

Checkout financing follows the same logic. McKinsey notes that Pay-in-4 providers use merchant checkout as a low-cost acquisition channel because the user is already inside a live purchase moment.

Educational content has a larger role here than in simpler products. It reduces anxiety, clarifies tradeoffs, and helps users understand the action they are about to take.

Referral programs need different design in high-risk categories. Research in the Journal of the Academy of Marketing Science shows that referral incentives should account for product recommendation risk, because some recommendations create reputational risk for the referrer. In fintech, where a bad recommendation can affect money or trust, two-sided or recipient-focused rewards are often safer than simply paying the existing user to invite someone else.

That means referral programs should not be copied from low-risk consumer products.

A good fintech referral gives both sides confidence. It should explain who the product is for, what the first action is, what the risks are, and why the recommendation is appropriate.

The most reliable fintech acquisition patterns

Across the research, several patterns appear repeatedly.

1. Reduce anxiety before asking for action

Fintech content should not only explain features. It should reduce perceived risk.

Good content answers questions users may not ask out loud:

- Is this safe?

- What happens to my money?

- What does the company do with my data?

- What happens if verification fails?

- Why do I need to deposit now?

- What fees or risks should I understand?

- How do I get support?

This is especially important for crypto, investing, lending, wallets, and cross-border finance.

2. Target inflection points

Fintech adoption is often event-driven.

Graduation, relocation, employment, rate changes, market cycles, debt refinancing, merchant onboarding, first payroll, and large purchases create moments where users are more open to switching.

A generic campaign asks for attention. An inflection-point campaign meets a user when the problem is already active.

3. Build around the first monetizable action

The signup is rarely the point.

For each product, the team should define the first action that creates value:

- first deposit,

- first trade,

- first transfer,

- first repayment,

- first card transaction,

- first merchant payment,

- first payroll switch,

- first financed checkout,

- first recurring use.

Then acquisition, onboarding, messaging, lifecycle, and creator campaigns should move toward that action.

4. Use embedded distribution where possible

If the product can sit inside an existing workflow, that usually beats asking users to form a new habit from scratch.

Embedded finance, merchant integrations, payroll partnerships, vertical SaaS, marketplaces, and wallet integrations can all reduce acquisition friction because they place the product near live intent.

5. Treat creator and referral growth as trust transfer

Creators, KOLs, communities, and referrals work best when they transfer credibility.

They underperform when they only create exposure.

This is especially true in crypto and investing, where users need interpretation, not only awareness. The creator must be trusted by the audience, understand the product, and explain the use case without overstating it.

Green Dots Research documents what we see across Web3 GTM strategy, creator-led distribution, founder growth, user acquisition, and market adoption.

Subscribe to get new field notes when they go live.

What fintech teams should measure beyond CAC

CAC is useful, but fintech teams need a deeper view of acquisition quality.

A better fintech acquisition dashboard should include:

- cost per signup,

- cost per verified user,

- cost per funded user,

- cost per first transaction,

- cost per repeat transaction,

- KYC completion rate,

- first-deposit rate,

- time to first value,

- day-7 and day-30 retention,

- primary relationship indicators,

- referral quality,

- channel-level payback,

- and cohort-level revenue.

This matters because the cheapest user is often not the best user.

A cheap signup that never funds the account is not efficient. A low-CAC referral that churns after an incentive is not durable. A paid user who becomes primary, transacts repeatedly, and refers others may be more attractive even if the initial acquisition cost is higher.

The practical takeaway for fintech growth teams

Fintech user acquisition should start with a sharper question: What trust barrier must be crossed before this user takes the first valuable action?

That question changes the work.

For paid acquisition, it forces teams to focus on intent and landing experience.

For SEO and content, it forces teams to answer real user anxieties rather than publish feature explanations.

For partnerships, it forces teams to find distribution nodes near the moment of need.

For KOLs and creators, it forces teams to choose credibility and audience fit over reach.

For product, it forces teams to remove onboarding friction before scaling traffic.

The best fintech growth systems are built around trust, timing, and activation. Channels matter, but they matter inside that system.

Subscribe to get new studies, frameworks, and field notes from Green Dots Research.

Author note

Written by Stacy Muur, founder of Green Dots. Green Dots works with Web3 teams on GTM strategy, creator-led distribution, founder growth, and launch architecture.